![]() ISSN: 1885-8031

ISSN: 1885-8031

https://dx.doi.org/10.5209/REVE.88655

La vulnerabilidad financiera en las entidades sin ánimo de lucro: propuesta de un marco teórico

Inmaculada Jimeno García[1]![]() ,

Anne Marie Garvey[2]

,

Anne Marie Garvey[2]![]() ,

Carlos Mir Fernández[3]

y Rocío Flores Jimeno[4]

,

Carlos Mir Fernández[3]

y Rocío Flores Jimeno[4]![]()

Recibido: 11 de octubre de 2022 / Aceptado: 9 de mayo de 2023 / Publicado: 21 de agosto de 2023

Resumen. Las entidades que forman parte de la economía social se han creado para dar respuesta a las necesidades sociales. Son muchas, por otra parte, las que cierran cada año tras un periodo de dificultades financieras. Dada la importancia que tanto a nivel social como económico tienen estas entidades, el estudio de su vulnerabilidad financiera es un área de especial interés, no sólo para destacar los factores que caracterizan a este tipo de entidades en dicha situación, sino como una forma de anticipar situaciones futuras que puedan no ser deseables. De esta manera, la propia entidad podría hacer frente a los cambios necesarios en su estructura y en su gestión con la idea de reconducir su gestión. En nuestro trabajo, a través de un análisis detallado de los diferentes trabajos académicos que analizan dicha vulnerabilidad, construimos un pentagrama que representa las cinco dimensiones – algunas interrelacionadas – o elementos que deben ser tomados en consideración en el estudio de su vulnerabilidad, a saber, el desempeño, la dimensión operativa, el apalancamiento, la liquidez y, sobre todas ellas, la reputación. Esta investigación ofrece una propuesta para evaluar la vulnerabilidad financiera en las ESAL de una manera más integral y facilitar su gestión.

Palabras clave: Entidades sin Ánimo de Lucro; ESAL; Vulnerabilidad Financiera; Rendimiento; Dimensión operativa; Apalancamiento; Liquidez y reputación.

Claves Econlit: L30; M00; M410; G33; B55; A13.

[en] The financial vulnerability of non-profit entities: A theoretical framework proposal

Abstract. NPOs (Non-Profit Organisations) are entities created to respond to the social needs of the economy, many of which fall into financial difficulties and are forced to close. Given the importance that these entities have both socially and economically, the study of their financial vulnerability is an area of special interest. It is important to highlight the factors that characterize this type of entity in a situation of vulnerability and also to anticipate future undesirable situations which could result in closure without timely supervision. In this way, the entity could redirect its management and make the necessary changes in its structure to ensure its continuity. Our study analyses the academic literature, from a theoretical perspective, in relation to this vulnerability allowing us to construct a pentagram of five dimensions, some interrelated, which we propose to be taken into consideration in the study of an entity’s vulnerability. These five dimensions are performance, operational dimension, leverage, liquidity and most importantly reputation. This research offers a proposal to evaluate financial vulnerability in NPOs in a more comprehensive way and facilitate its management.

Keywords: Non-Profit Organisation; NPO; Financial Vulnerability; Performance; Operational dimension; Leverage; Liquidity and reputation.

Summary. 1. Introduction. 2. For-profit and non-profit organisations in the face of financial vulnerability. 3. Definition of financial vulnerability in non-profit entities. 4. Relevance of the indicators in NPOs. 5. Dimensions and variables to study financial vulnerability in NPOs. 6. Conclusions. 7. References.

How to cite. Jimeno García, I., Garvey, A.M., Mir Fernández, C. & Flores Jimeno, R. (2023). The financial vulnerability of non-profit entities: A theoretical framework proposal. REVESCO. Revista de Estudios Cooperativos, 1(144), e88655. https://dx.doi.org/10.5209/reve.88655.

Non-profit entities are organizations that have been created to respond to social needs, those that are not attended to by either the public or private sectors (Corral-Lage, Maguregui-Urionabarreneches and Elechiguerra-Arrizabalaga, 2019; Chaves and Monzón, 2018; Solana et al., 2017), which is why a residual field arises, called the third sector (Salamon, L., & Anheier, 1996). This type of entity has a general interest purpose (Socias Salvá, 1999) and are independent from public administrations (Corral-Lage & Peña-Miguel, 2016), but highly dependent on income from donations and have little financial autonomy. The relevance of these entities can be seen internationally by the number of organizations that exist, in the employment they generate, in the social needs they cover and in the number of beneficiaries they serve (Martínez & Guzmán, 2014).

In the period of the economic crisis that began in 2008, the functioning of the welfare state was questioned (Martínez & Guzmán, 2014) and, to a large extent, its inefficiency was covered by this third sector, protecting a dissatisfied part of the population. In fact, this sector was faced with unprecedented challenges of pursuing sustainable development (Hu and Kapucu, 2015). In this context, public entities, donors or benefactors and society in general have been demanding more transparency and control mechanisms to ensure the correct use of the scarce resources received by these organizations (Bellostas, Brusca, & Moneva, 2006; Marcuello Servós, et al., 2007; Corral et al., 2014; Martínez and Gúzman, 2014). These control tools have been evidenced both nationally and internationally through a dispersed regulatory framework in corporate information and at a social level (Briones Ortega, 2015).

However, this increase in control tools has not been supported by an increase in funding. In this sense, the scarcity of economic resources to meet society’s demands has been and is the main concern of the sector.

The sustainability and economic stability of this type of entity is based on the fact that its main source of financing comes from its own resources and generally has a low level of indebtedness (Martínez and Guzmán, 2014), together with good governance and transparency management. Traditionally, these entities were highly dependent on public financing, but this is gradually changing. Nowadays, private financing plays an important role in the search for diversification in obtaining resources, to avoid dependencies which could jeopardize the financial structure of the entity. In addition, the collaboration between entities in this sector together with other public and private sector entities helps to facilitate the adaptation to the current digital society and to attract and maintain talent. The non-existence of a profit objective should not be confused with the non-existence of management within the organization (Maguregui Urionabarrenechea, Corral Lage, & Elechiguerra Arrizabalaga, 2015).

In this sense, non-profit entities (NPO hereinafter), which boast good management of available resources and offer transparent information on the entity, achieve greater legitimacy as an organization and as a social entity (Marcuello Servós et al., 2007; Carvalho et al., 2017; Martín and Martín, 2020) and, therefore, a good management capacity over time. Therefore, transparency together with accountability becomes a channel for obtaining financing.

Unfortunately, many NPOs close each year and most of these closures are preceded by a period of financial difficulties (Searing, 2017), but there is a general absence of legal registers relating to bankrupt NPOs (Hager, 2001; Prentice, 2016a). For this reason, assessing the financial vulnerability of organizations is increasingly important (de Andres-Alonso et al., 2016). In fact, analysing these organizations makes us aware of signals indicating that an entity is in difficulty and the reasons for the problems found (Giner & Gill de Albornoz, 2013). In this way, the entity itself could face the necessary changes in its management to redirect the situation (Lu et al., 2020). Of course, we must distinguish between financial failure, financial vulnerability and closure of NPOs when the objective they started out to achieve in the first place is reached. Our paper looks at financial vulnerability and its management. We therefore examine cases of financial failures because these were entities which were financially vulnerable before they failed and a mechanism to manage that vulnerability on time could have prevented the closure of the entity. In fact, good management procedures to prevent financial vulnerability can aid NPOs success in general.

Logically, it is necessary at this point to determine what we understand by the financial vulnerability of an organization when conducting a study of these characteristics, since it is a concept underlying the work involved to detect and anticipate its detection (Flores-Jimeno & Jimeno-García, 2017). Until now, previous literature has focused mainly on detecting which indicators show signs of financial vulnerability (de Andres-Alonso et al., 2016), even within the macroeconomic sphere (Adrián, Boyarchenko & Giannina, 2019), and not on establishing a theoretical framework on the subject in question to serve as an umbrella for future developments. As in the lucrative field, numerous contributions have been made in this line, although there has not been a consensus on a single theory on business failure or on the factors that determine it (Mateos et al., 2011). The definition of financial vulnerability is far from clear within the academic community, which adds to the difficulty of measuring organizations classified as inactive or defunct (Hager, 2001).

For this reason, the objective of this research is to identify a system of classification or characterisation that exists in relation to the financial vulnerability in these organizations. We respond to this by examining this broad concept of vulnerability and focus on classifying it into subsections which can assist when making a diagnosis. The former is done taking into consideration the wide spectrum of interrelated elements. We perform a detailed analysis of academic bibliography that analyses this said vulnerability and advance to build a pentagram that represents the five dimensions included in the literature which are considered key to creating a starting point to this theoretical framework: performance, operational dimension, leverage, liquidity and, above all, reputation. This research is timely and is a step forward in the proposal to avoid failure in NPOs through financial analysis and management.

The paper continues as follows, in the next section we carry out a study on the general concept of financial vulnerability, both for profit and non-profit entities. In the third section we analyse the specific vulnerability of non-profit entities. The fourth area analyses the different dimensions that define financial vulnerability. The fifth part of the study deals with the relevance of indicators in NPOs. Finally, we present the dimensions and variables of our financial vulnerability model and offer conclusions in the seventh section.

2. For-profit and non-profit organisations in the face of financial vulnerability

In previous literature where the financial vulnerability of organizations is studied, analysed and attempts were made for an advanced diagnosis, we consider that the definition given to the dependent variable is fundamental (Flores-Jimeno & Jimeno-García, 2017). The definition defines the concept and is the foundation on which all research is built. In the case of for-profit organizations, the main event used as a definition is usually different depending on the objective of the model and the research intention (Balcaen & Ooghe, 2006). This constitutes a difficulty when comparing the results from different studies.

More specifically, some studies simplify the concept of business failure by associating it with a specific moment in time, which usually coincides with the legal definition (Altman, 1968; Mckee, 2000; Ohlson, 1980; Taffler, 1984; Zmijewski, 1984), subject to, for example, the requirements contemplated in the bankruptcy regulations for liquidation processes (See Art. 460 et seq. of RDl 1/2020, of May 5, which includes the revised text of the Bankruptcy Law). It is important, however, to focus more attention on economic and financial failure, leaving legal failure in the background (Gazengel and Thomas, 1992). Many studies link a loss to behavioural variables, such as, for example, the relationship between accounting data and future solvency (Laffarga J. and Mora, 1998). They use a static methodology to study this phenomenon. In fact, they focus on examining which variables best identify failure and distinguish between healthy and failed companies, involving an analytical vision in the short term (Altman, E., Iwanicz-Drozdowska, M., Laitinen, E., & Suvas, 2015), looking for specific points in time in the data to identify when the frustration in the entity actually occurred.

However, business failure is not a sudden event. It is a process that, prolonged in time, as a consequence of not taking adequate measures to correct the situation that causes instability, can lead to the interruption of the entity's activity (Altman, 1968; Argenti, 1976; Laitinen E, 1991; Lukason, 2012; Ooghe & De Sofie, 2008; Lukason and Vissek, 2018; Lukason and Laitinen, 2019; Laitinen, 2021). Understanding that business failure is a process of financial struggle, its reality cannot be simplified by analysing certain variables and by using a static methodology, but its evolution over time needs to be studied and contemplated and thus the continuous management of financial vulnerability is essential.

If we take this evidence from the existent research base within the lucrative sphere and project it to the definition of success or failure in an NPO, we are faced with a complex problem due to the peculiarities of these entities. NPOs are characterized by their orientation towards achieving social objectives, so an indicator of success is the achievement of the objectives proposed (Helmig et al., 2013), going beyond the measurement of certain financial variables, such as economic performance. NPOs are entities driven by moral values and in which there is a high component of volunteerism, so it is crucial that a high degree of agreement is reached within the organization itself and a vision of its aims and the results to be obtained are shared (Mataix Aldeanueva, 2001).

As anticipated, we must assume that financial difficulties are common in NPOs (Tevel et al., 2015 and Searing, 2017), adapting the social services offered to financial capacity in the short term. Some entities are dissolved due to financial difficulties, and yet others recover despite adversity. The data show that the ability to carry out its function is above the resources captured on the basis of efficiency criteria by management (PwC, 2018).

The difference between dissolving or saving the entity resides in how these organizations are managed (Tevel et al., 2015). There are very few studies on this subject, so we have a very limited understanding of the dynamics that lead to the disappearance of these entities (Fernandez, 2008). In fact, due to the particular circumstances of entities in this sector, it is more difficult to associate financial vulnerability with the moment of failure. The overall vision and the entity’s mission may be relevant (Mataix Aldeanueva, 2001). More specifically:

– In the first place, one of the main differences between both sectors is in the availability of financial information. The information issued by NPOs is limited. In turn, the reception that interest groups have of this information is more asymmetric than it is for-profit companies (Hofmann & McSwain, 2013). Different stakeholders have different concerns about management and accountability. This limitation may have its origin in the specific requirements established by the authorities that regulate associations and foundations (common legal forms of NPOs), since they are exempt from certain taxes, they do not need to be part of capital markets. They also have an accounting framework adapted to NPOs, which is generic and caters for the complexity of these entities and which adapts to the diversity of circumstances that these entities have. Of interest is the fact that larger NPOs perform better management as they have more access to activity management and control mechanisms (Ye and Gong, 2021), which help them to take management decisions to reach the end of the financial year with results that don’t question their survival.

– Secondly, we have to take into consideration the disparity between the objectives of both types of organizations. Profit maximization is sought in profit-making entities. While NPOs seek to maximize services to society from the most efficient management possible of the resources available to them in the short term.

– Finally, we must also take into account the different forms of financing that these two sectors have. Funding sources for NPOs are usually member contributions, donations and grants. While, in profit-making companies, their sources of financing are from capital contributions and loans.

In short, from the differences discussed, we understand that the most important are found in the origin of their capital and the purpose pursued by their contribution (Rodríguez Martínez, 2005). The nature of the NPO's mission and its sources of financing make it more accountable (Abraham, 2003). Therefore, financial responsibility and accountability are two fundamental issues in NPOs that should be developed further. In fact, both arise as a consequence of both external demands and internal needs.

These differences mean that the predictive measures of profit-making organizations cannot be applied to non-profit organizations. In fact, there has been a need to adapt the for-profit literature to the financial situation of NPOs (Green et al., 2021). However, it is possible to estimate the results they have had in both types of organization, although they do not provide us with the same meaning for the purposes of our study.

In an NPO, the priority is not to measure profitability, but to analyse the degree of compliance with the objectives established in its budget (Rodríguez, 2005), since its purpose is to provide its beneficiaries with the highest quantity and quality of services possible, depending on the availability of resources (González & Rúa, 2007; Ibáñez & Benito, 2013). For this reason, it is not feasible to use profitability as a performance measure (Martínez and Guzmán, 2014), since a profit distribution objective is not established (Grosso, 2013). In fact, obtaining a profit may mean that efficient management was not carried out, and opportunities were lost when providing services (Arnau, Fuertes, & Maset-Llaudes, 2007). Although, on the other hand, the generation of surpluses gives these organizations financial stability and room for reaction to the possibility of loss of financing sources in the future. However, the main objective of NPOs shows the need to look for alternatives to evaluate performance (Ibáñez & Benito, 2013).

NPOs face the double task of achieving the objectives related to their mission, while maintaining a healthy - or at least adequate - financial condition that guarantees their survival (Carroll & Stater, 2009). It is true that if an organization has a good system of financial responsibility, it will be easier and more foreseeable to bear a financial shock. In fact, an adequate accounting system can help the organization to take action at the right time (Abraham, 2003). Aguado et al., (2021) shows the feasibility of introducing a social accounting method in a corporation belonging to the social economy able to produce information valid to understand and align the value that each organization produces with stakeholders’ interests and the wellbeing of the community where the corporation operates.

It is also important to bear in mind that in the non-profit sector, alternative measures for similar concepts can be found when analysing the financial health of these entities. This lack of homogeneity is what generates discrepancies when determining the specific fact that constitutes organizational failure or, rather, which fact is what determines the condition of vulnerability in non-profit organizations (Searing, 2017).

3. Definition of financial vulnerability in non-profit entities

The definition of financial vulnerability in NPOs is not clear among academics according to de Andrés-Alonso et al., (2015), as their equity structure may not be decisive. These are entities highly dependent on public resources, with high levels of funding from private donations, and less subordination from private funding (Pardo & Valor, 2012).

In general terms, financial vulnerability can lead to the disappearance of an entity due to financial problems and its inability to continue providing its social objective. In fact, if the entity is in a situation of vulnerability and is not capable of adapting to these circumstances or redirecting the said situation, it may finally disappear (López-Arceiz et al., 2017), which can lead to legal failure. Therefore, we define the failure of the organization as its deterioration in adapting to its changing environment with the consequent reduction of resources associated with this situation. Lack of income (due to the loss of an important benefactor or group of donors) or poor management by the organization - smaller NPOs have more difficulty adjusting expenses to changes in income – which can cause them to stop meeting social objectives (Ye and Gong, 2021). This economic slowdown can lead to financial problems, a situation that over time can lead to the dissolution of the entity (Flores & Jimeno, 2019).

Firstly, this definition has to be focused specifically on non-profit entities due to their characteristics. In the first place, when giving up profit in the form of performance, it makes no sense to speak of failure from a strictly economic point of view. As we have already commented, its objective is the achievement of social goals and not the maximization of profit. This does not mean that, in order to have good financial health, these entities need to generate some surpluses and incorporate them as reserves but is an issue that requires further research as maintaining a certain reserve would help in the management of financial vulnerability when it arises. In fact, to achieve their objectives, they have to manage their resources in the best way possible and when this is not the case, sooner or later they will end up having financial problems.

Secondly, it is true that entity dissolution can be a consequence of the failure process but equating the failure of the organization to its dissolution can pose a number of problems (Helmig et al., 2013). Some authors understand that the disappearance of an NPO does not have to be understood as a failure of the said entity. In fact, it can sometimes happen that these entities stop operating when they have fully fulfilled their mission (Fernandez, 2008). However, the disappearance may also be due to a situation of insufficient resources or from the poor management of available resources... Or that, at a time of economic slowdown, it is necessary to reduce the offer of its services because it has suffered the loss of an important benefactor or a group of donors (Elbers & Arts, 2011; Greenlee & Trussel, 2000). However, good resource management, as well as analysing the financial situation of the organization can help these entities readjust to complex situations and even survive them.

It is difficult to measure the extinction and inactivity of these organizations (de Andres-Alonso et al., 2016), since it can be understood in different ways. In the previous literature there are multiple definitions (see Thomas and Trafford, 2013) which elaborate a Financial Exposure Index (FEI) by applying the mean (arithmetic and geometric) of the four original variables by Tuckman and Chang (1991). Despite the efforts of researchers to develop objective indicators and measuring NPO’s financial health, currently there is no consensus on what financial health is and how it should be measured (Hung & Hager, 2019; Park, Shon and Lu, 2021).

Table 1 includes the variables used for the definition of vulnerability, however none of them is absolutely complete. In fact, according to Searing (2020) there are inconsistent definitions for the disappearance of non-profit entities. Gilbert, Menon, & Schwartz (1990) define the financial vulnerability of an organization as the accumulation of losses by the entity over three consecutive years. In NPOs it is understood that financial problems arise due to similar issues but are not related to profit or loss, for example when there is a reduction of funds for three consecutive years (Tevel et al., 2015). Thomas and Trafford (2013) elaborate a Financial Exposure Index using the mean (arithmetic and geometric) of the four original variables disclosed by Tuckman and Chang (1991).

Table. 1. Definition of vulnerability and variables used in non-profit entities

|

Authors |

Definition of vulnerability |

Variables |

|

Gilbert, Menon, & Schwartz (1990) |

Accumulation of losses for three consecutive years |

- |

|

Tuckman y Chang (1991) |

Decrease in services provided in the face of a financial shock |

Debt ratio Net assets Administrative costs Operating margin |

|

Greenlee y Trussel (2000) |

Decrease in programmed expenses during three consecutive periods |

The same variables as Tuckman & Chang (1991) |

|

Trussel (2002) |

Decrease in funds by more than 20% for three consecutive years |

Debt ratio Income concentration index Operating margin The size of the organization The sector |

|

Trussel, Greenlee, & Brady, 2002 |

Net asset reduction over three consecutive years. |

Debt ratio Income concentration index Operating margin[5] Administrative costs The size of the organization (natural log of total assets) |

|

Greenlee & Trussel, (2004) |

Overall decline in funds for three consecutive years |

Tuckman y Chang (1991) |

|

Keating et al. (2005) |

Asset reduction Reduction of programmed expenses Technical insolvency Interruption in financing |

They compare the usefulness of the variables used by Tuckman and Chang (1991) with the variables used in other models by for-profit entities such as those used in the study by Altman (1968) and Olshon (1980) |

|

Bowman (2011) |

It does not define financial vulnerability. Defines financial performance (financial capacity and sustainability). |

Indicators that measure short-term and long-term financial capacity: Monthly expenses = (Assets without financial restrictions - Unsecured debt) / Expenses in operations Debt ratio Indicators that measure short-term and long-term financial sustainability: Margin = (Unrestricted Income + Net Assets released from Restrictions - Total Expenses + Depreciation) / (Total Expenses - Depreciation) ROA |

|

Cordery, Sim, & Baskerville (2013) |

Compare and contrast different definitions based on programme spending, assets, and net earnings or income concentration. |

They disclose three models: Based on the model disclosed by Tuckman and Chang (1991) Another model that follows the line disclosed by Trussel (2002), Greenlee and Trussel (2004), Trussel et al., 2002) The third is based on a model of net earnings or income concentration (Carroll & Stater, 2009; Chang, CF, & Tuckman, 1994; Fischer et al., 2011; Froelich, 1999; Gilbert et al., 1990; Hodge & Piccolo, 2005; Keating et al., 2005; Wicker et al., 2012) |

|

de Andrés-Alonso et al. (2015) |

They use the definition proposed by Trussel et al. (2002). |

FVI defined by Trussel et al. (2002) |

|

Tevel et al. (2015) |

Significant decrease in funds for three years. |

Three models: the Olshon model (1980), the Tuckman and Chang model (1991) and the professional model. |

|

de Andrés-Alonso et al. (2016) |

Three different dimensions; operating, leverage and liquidity. |

Net assets Financial leverage Liquidity |

|

Prentice (2016b) |

Research that considers the number of financial measurements to capture accounting ratios. |

Liquidity, Solvency, Margin, and Profitability |

|

Searing (2017) |

Two definitions: bad debt (liabilities exceed assets) and financial disruption (when net assets are reduced by more than 25%). |

Debt ratio Net assets Operating margin Size Years |

|

Green et al. (2021) |

Rationale and expected sign in relation to survival probability[6] |

Sufficient equity: Months of asset cover (net assets /income x 12) Financial concentration: Herfindahl Index Administration cost: Staff costs as a percentage of total income Margin: Total cost as a percentage of total income |

|

Park, Shon and Lu (2021) |

Review the dimensions of nonprofit financial health (in Bowman et al., 2005, and Prentice, 2016b) that provide the basis for validating financial measures against nonprofit dissolution |

Solvency Profitability Margin: surplus/deficit normalized by total revenue in a year Liquidity |

Source: Own elaboration

In the research mentioned by Tuckman and Chang (1991) in which the vulnerability of NPOs is evaluated from accounting variables, we find the first definition of financial vulnerability for these entities. These authors define vulnerability as the decrease in services provided in the face of a financial shock, although due to the methodology they used, it was not necessary for them to measure this concept when conducting their study. The authors considered that an organization is in a situation of financial vulnerability, when at least one of the four variables they analysed was in the bottom quintile: sources of income (benefactors and their instability), net assets, administrative costs and operating margin.

This study was followed by others such as Greenlee & Trussel (2000), Trussel (2002), Greenlee & Trussel (2004). Greenlee & Trussel (2000) propose a first predictive model, making the concept of financial vulnerability operational, defining it as the continuous decrease in programmed expenditures during three consecutive years.

Subsequently, Trussel (2002) defines vulnerability as the decrease in funds by more than twenty percent over three consecutive years. In this way, it is ensured that there really is a financial decrease. Greenlee & Trussel (2004) use a similar definition, since they conceive this concept as a general reduction of funds for three consecutive years, they understand that it can be translated into a lower amount of income or an increase in expenses with the consequent reduction of services (from Andres-Alonso et al., 2016). And, therefore, if the provision of services is reduced, the entity may not be able to fulfil its mission (Trussel, Greenlee, & Brady, 2002).

In subsequent studies, these vulnerability definitions have been used together to analyse whether a situation of financial risk can be predicted in these entities (de Andres-Alonso et al., 2016). Although, in these latter studies new concepts of vulnerability have also been introduced.

In the study by Keating et al. (2005) four concepts of financial vulnerability are analysed. On the one hand, the (significant) reduction in net assets and the reduction in programmed expenses are analysed, with a reduction of at least 25% in one year for both concepts. And, on the other hand, two new concepts of financial vulnerability are introduced: the concept of technical insolvency[7] and financial disruption[8].

Previous literature, such as Cordery, Sim, & Baskerville, (2013), by Andrés-Alonso et al. (2015), Searing (2017), Tevel et al. (2015) follow this same line, showing different definitions of vulnerability, although they continue to do so in a fragmented way. In other words, their models do not include a multidimensional definition of what financial vulnerability is. These studies tested their models independently, without looking for coincidences with organizations that are considered financially vulnerable from their different dimensions (de Andres-Alonso et al., 2016). However, Bowman (2011) elaborates the first alternative model to the traditional one by Howard P. Tuckman and Cyril F. Chang, (1991) for NPOs. Bowman (2011) does not define financial vulnerability in his model, but he does introduce two concepts that are related to financial performance; on the one hand, it refers to financial capacity and, on the other, to financial sustainability. Financial capacity is understood to be the resources available to the organization to face the opportunities it has or to react to possible threats. And financial sustainability is defined as the rate of change in financial capacity in each period. It can be said that this model is the first to encompass different dimensions from a dynamic point of view in terms of financial performance.

Along similar lines, the research carried out by de Andres-Alonso et al. (2016) defends that financial vulnerability is a concept that encompasses several dimensions. In fact, we see that there is a need to define financial vulnerability from all its meanings in order to form constructive and comprehensive conclusions. In this sense, the research carried out by de Andres-Alonso et al. (2016) already takes a very important step in this line of study. It specifies that financial vulnerability must be studied from three dimensions: the operational, leverage and liquidity dimension. In this way, Park et al. (2021) reviews four different dimensions of non-profit financial health (solvency, profitability, margin and liquidity) and their result provides important implications. They discovered that higher solvency, profitability, and margin have significant effects on reducing non-profit dissolution.

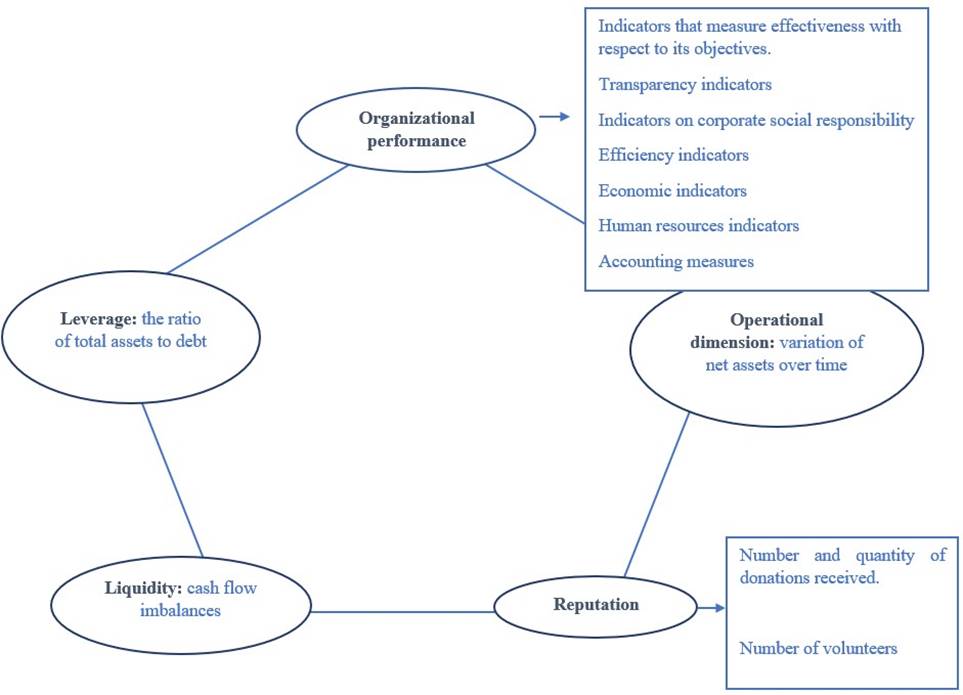

From our point of view, this definition of vulnerability by Andres-Alonso et al. (2016) and Park et al. (2021) based on three and four dimensions respectively would be incomplete. We consider that two very important and essential components to analyse financial vulnerability in non-profit entities are missing: organizational performance and reputation. These two dimensions are important factors that can generate vulnerability in this type of entity. Therefore, if we take into account indicators reflecting these two factors when analysing the situation of NPOs, it can give us valuable information on the entity's vulnerability risk.

Organizational performance is the organization's ability to acquire and process resources to achieve its objectives (Madella, Bayle and Tome, 2005). According to several authors, it is a concept that takes into account financial, non-financial and intangible aspects (Muthuveloo, Sharmugan and Teoh, 2017; Tseng and Lee, 2014). Therefore, organizational performance can give us a vision as to whether the entity is efficiently managing the resources it has available (Martínez & Guzmán, 2014), a relevant question to ensure the entity’s survival.

On the other hand, previous literature highlights that reputation is a determining factor when it comes to attracting both donations and volunteers (Meijer, 2009; Schloderer, Sarstedt, & Ringle, 2014). A previous study which analysed business reputation in a particular business industry, and which could also be considered for NPOs in general, highlighted that the quality of the services offered, the organizational culture and corporate values and finally the sense of belonging to the organisation were considered to be important issues for reputation (López-Santamaría et al., 2021). In fact, we must bear in mind that these entities depend both on the donations they receive and, on the activity carried out by volunteers. Donations are their main source of funding (Pardo, E., & Valor, 2012) and the activity of volunteers, both individual and corporate (Ibáñez & Benito, 2013), is a fundamental source of labour when developing their mission. Therefore, both factors are essential and of vital importance for the survival of the entity (Comyns & Franklin-Johnson, 2018; Gent et al., 2015; Schloderer et al., 2014). And therefore, NPOs need to develop and strengthen their own reputation (Tremblay-Boire et al., 2016).

Reputation as a social construct is an important aspect for the organization. More specifically, in the organizational strategy, as it influences the perception of organizational effectiveness and, in the success of obtaining resources (Santos et al., 2019). In short, reputation is an asset to the organization (Comyns and Franklin-Johnson 2018), which can have positive or negative impacts depending on the management carried out. In fact, cases of fraud, corruption, inefficient management or opportunistic practices in these types of entities cause them to lose part of their income (Burger, 2012; Santos et al., 2019).

Therefore, we understand that financial vulnerability is a long process in time, and that, if the entity does not manage to redirect this situation, the initial circumstances will worsen over time. This means that the capacity of the organization deteriorates, and its viability is threatened. This process has to be studied from the different dimensions that make up the pentagram: the analysis of organizational performance, operational vulnerability, leverage, liquidity and the reputation of the organization.

4. Relevance of the indicators in NPOs

The Prentice (2016b) financial indices are those traditionally used to predict and diagnose financial vulnerability (Searing, 2017), something that undoubtedly has a clear application in both for-profit and non-profit entities. It is a continuous method of measuring financial performance over time and measuring the effect on equity and ongoing management. In this regard, previous literature shows us that the use of financial ratios in predicting the financial vulnerability of NPOs, although it does not provide us with any guidance on how to orientate the entity’s efforts towards recovery, is something that will remain important for future decision making in this type of entity. In fact, it should be possible to use this knowledge to make both predictions about vulnerability and to manage the survival of the organization (Searing, 2017; Searing, 2021). Numerous findings have been made regarding this topic, although some of them are ambiguous and contradictory (Ashley & Faulk, 2010; Bhattacharya & Tinkelman, 2009; Cnaan et al., 2011).

However, the characteristics of NPOs lead us to conclude that in addition to financial indicators, other types of markers are necessary to study the financial vulnerability of these entities, markers which are different to those commonly used in profit-making entities. If we focus on the characteristics of these entities, we must firstly highlight the purpose they seek, which defines their primary objective: to provide a social benefit, that is, they provide their beneficiaries with the greatest quantity and quality of services possible with the limited resources available to them (Andersen and Petersen, 1993; Charnes et al., 1997; González & Rúa, 2007; Coupet and Berrett, 2018), and where maximization of results is not found in monetary terms. This affects the study of their vulnerability, since profitability analyse or other economic ratios as a measure of performance of these entities is unnecessary (Martínez and Guzmán, 2014). However, it needs to analyse how they distribute the available resources when providing their services. The way to carry out this analysis should focus on whether these entities are being managed efficiently (Martínez and Guzmán, 2014).

There is a current academic debate regarding what is understood by efficiency and effectiveness in NPOs, as well as what are the best ways to measure these aspects (Hernangómez, et al., 2008; Solana et al., 2017; Coupet and Berrett, 2018). In fact, the efficiency assessment shows serious difficulties (Hernangómez, et al., 2008) especially if it is done in the traditional way, using production and cost (Ibáñez & Benito, 2013) in purely monetary terms. Specifically, a first difficulty is the establishment of a standard or value reference that is considered adequate to make comparisons with the values obtained. A second difficulty is to measure efficiency with an adequate precision in organizational contexts which have multiple dimension objectives - outputs - and the resources used - inputs - (Hernangómez, et al., 2008; Coupet and Berrett, 2018).

By way of example in this area and for the case of Spain, the Asociación Española de Contabilidad y Administración de Empresas (AECA, 2010) states that the economic-financial information must allow users to perceive whether the entities are effective and efficient in terms of their management. The result of the former means that an important part of the indicators used to analyse their viability must come from transparent financial statements. Along the same lines, (AECA, 2012) recognizes that indicators are nothing more than instruments for measuring both quantitative and qualitative aspects, which can be used as an objective guide for comparison or measurement to put in order, control or assess any reality, attribute or provide information that has a clear purpose of formally and synthetically obtaining a result with reference to a previously defined time horizon. Among these indicators we find liquidity, cash flows and solvency.

However, and despite the usefulness of this financial information - a reflection on its transparency and the basis for an adequate image or reputation - some authors such as Ibáñez & Benito (2013) state that we cannot stick to data extracted from income statements. The inputs of the process - the costs - we can obtain from a traditional profit and loss account; however, the outputs cannot be measured from the income obtained in that accounting statement. To measure them, it would be necessary to introduce aspects that are related to the social value that these entities generate. In fact, some authors propose to substitute production and output indicators for social economic result or social impact. Along the same lines, (AECA, 2012) incorporates condition indicators that measure efficiency[9] in relation to its objectives, such as indicators assessing the capacity for self-government or the application of surpluses for non-profit purposes, or, for example, indicators of transparency or corporate social responsibility; (José González Quintana, 2003) incorporates a series of indicators such as: efficiency indicators, which compare the services provided with their cost, economy indicators, which measure, for example, the average number of workers for each activity, or human resources indicators.

Likewise, some of the accounting measures that have been used in the previous literature and that are disclosed in research work by Hernangómez, et al. (2008) to measure efficiency are, for example, price or project spending. The price is defined as the cost to each benefactor to acquire a monetary unit of output for the beneficiaries. And project expenditure refers to project expenditure relative to total expenditures. Other similar, widely used measures are, for example, technical efficiency – the percentage that represents administrative expenses over total expenses - and efficiency in allocation – the percentage that represents expenses in projects over the total income of the entity (Hernangómez, et al., 2008; González & Rúa, 2007).

Martínez and Guzmán (2014) use total assets, liquidity ratio, indebtedness and seniority as variables to carry out the study of efficiency on a set of founding entities. The explanatory variables when measuring efficiency in a set of healthcare type foundations are total assets, liquidity ratio and seniority.

On this line of thought, we consult research by Solana, Ibáñez & Benito (2017), as it uses data from the annual accounts to measure the efficiency of a set of foundations. The variables that it selects to measure efficiency are, as inputs, the foundation endowment, total assets, total expenses and the number of employees, and as outputs, the number of beneficiaries and total income. The results of this study show that managers must put emphasis on their foundation endowment, assets, expenses and number of employees to improve their efficiency.

As we can see, in previous literature, proposals have been made to measure efficiency from both a technical and allocative perspective by using data provided by the annual accounts (González & Rúa, 2007). It is true that there are financial indices that can offer us information on efficiency (such as the proportion of expenses by programmes, fundraising and the cost of its collection), but it is also true that there are other indicators that provide us with information (Kim, 2017) on the stability (such as income concentration), capacity (such as liquidity), leverage and sustainability (operating margin). However, they should be measured with caution, given that although it is true that a higher concentration of income can lead to more financial vulnerability, having access to less concentrated sources of income increases the expenses of raising resources and in administration costs (Frumkin and Keating, 2011). In fact, these factors allow us to know what the organization's survival capacity is (Ryan & Irvine, 2012) and is a way of measuring organizational performance.

Secondly, the other characteristic that differentiates NPOs from other entities is the origin of their funds. In fact, these funds often come from member contributions, donations, and grants. Most of these funds come from domestic economies, so the image that these entities project on the activities they carry out is fundamental and has a direct impact on their reputation. Hence, the importance of taking into account image and reputation when analysing financial vulnerability. These entities use these sources of financing to meet their purpose, which is in the general interest. This, together with the absence of profit, shows that one of the entity's objectives is the efficient management of its resources, and therefore certain indicators used in its diagnosis of financial vulnerability must measure the optimal combination of resources applied / objectives achieved. Undoubtedly, efficient management of their resources allows them to obtain a greater return in the fulfilment of their social purposes.

NPOs obtain greater legitimacy when good management is practiced and offers more transparent information on the activity they carry out (Marcuello Servós et al., 2007). We must bear in mind that transparency is a fundamental and a necessary factor as a control mechanism, which is increasingly demanded by society (Corral & Elechiguerra, 2014; Marcuello, et al., 2007; Moneva and Bellostas, 2007). Unfortunately, these transparency requirements have not been reflected to the same extent in obtaining public funds (PWC, 2018), meaning a necessity to resort to a more efficient management of contributions. It should be noted that transparency criteria also results in the existence of better internal control measures, which, in the long run, allow for better management of this type of entity.

Hence the need to assess both the management and the reputation of non-profit entities. The objective of this evaluation is to improve the performance of the entities and, also, to increase confidence in them. By evaluating management, it is possible to learn about the impact that the said entity has on society and with this knowledge the proper application of the finance obtained by the entities can be guaranteed (Martínez & Guzmán, 2014). This gives visibility to the correct application of the funds received and greater confidence when making a donation (Golden et al., 2012). Hence the importance of offering information about the activity carried out, in a responsible, clear and legitimate way as it strengthens the image that society has with respect to the said entity.

We understand that both non-financial variables are relevant when conducting a study on the financial vulnerability of these entities. But these variables must be accompanied by the entity’s economic and financial data. Therefore, we make a proposal to study the NPO from different perspectives.

5. Dimensions and variables to study financial vulnerability in NPOs

In previous literature, financial vulnerability has been studied by examining one or more of its dimensions, without encompassing all of them. On the same lines as Andres-Alonso et al. (2016) and in accordance with the definition of financial vulnerability raised, a theoretical proposal is made for the study of financial vulnerability based on a series of variables that encompass the five dimensions previously described (organizational, operational performance, leverage, liquidity and reputation).

The first dimension is organizational performance. Through performance, we analyse whether the entity has a good relationship between its input - output in the broad sense, measuring whether an adequate application of the available resources is carried out when it comes to achieving its objectives. On proposing variables, we need to consider the limitations that variables determined on the basis of the income statement have (AECA, 2012; González Quintana, 2003), we should consider the following:

– Condition indicators that measure effectiveness with respect to its objectives, such as indicators for self-government capacity or the application of surpluses for non-profit purposes. They measure the degree to which corporate objectives are achieved, something complex to measure, and sometimes lacking a clear measurable objective to pursue.

– Transparency indicators (for example AECA, 2012):

o The functioning of governing bodies and their composition, the frequency of meetings and member participation at them, as well as the termination of mandates.

o Circularization of information, as well as the publication of ethical goals and values.

– Indicators on corporate social responsibility according to document nº 3 of AECA (2012): external opinions such as those of the auditor, on the environment and employment stability for the disabled.

– Efficiency indicators, which compare services provided with their cost, for example, the percentage that administrative expenses represent over the total expenses of the entity or the percentage that project expenses represent over the total income of the NPO. These indicators detect whether the process of transforming the resources into goods or services offered by the entity is carried out with an adequate level of performance. Maximization of output for a given level of input, or limitation of the inputs to reach a certain output.

– Economic indicators, which measure, for example, the average number of workers for each activity. They aim to reflect if resources have been acquired at cost, in a timely manner, quantity and quality desired for the purposes to be achieved. They can be applied at both the material, human and financial level.

– Human resources indicators (for example AECA, 2012): dedication of hired staff and volunteers, job stability, staff absenteeism.

Likewise, some of the accounting measures that have been used in previous literature and that are disclosed in the work of Hernangómez, et al. (2008) to measure efficiency are, for example, price or project spending. The price is defined as the cost for each donor to acquire a monetary unit of output for the beneficiaries. And project expenditure refers to project expenditure relative to total expenditure.

In relation to the operational dimension, some authors have defined it as the variation in revenues less expenses over time (de Andrés-Alonso et al., 2015; Cordery et al., 2013; Keating et al., 2005; JM Trussel, 2002; Greenlee & Trussel, 2004; Trussel et al., 2002). This dimension is undoubtedly associated with the variation in net assets. In this sense, the reduction in the organization's net assets over the years may be due to a decrease in income or an increase in expenses. When these variations persist and affect assets over time, they lead to serious operational problems in the organization. Andres-Alonso et al. (2016) advocate the use of net assets as a variable to be analysed and reject the use of margin, since they consider it a more volatile variable.

However, margin is one of the most used variables in previous literature, but it does not include all the aspects that measure operational vulnerability. For example, if there is a reduction in operating income and the organization decides to reduce its expenses in the same proportion, this variable would not be affected (García Rodríguez, 2017; Lizano et al., 2010). In this case, it is understood that the entity would be adjusting to the circumstances, adapting to the available resources, even using them more efficiently, increasing its services with more limited resources (PwC, 2018).

Finally, it is proposed to analyse this dimension over time and to do so using the variation in net assets as a variable. This operational dimension is undoubtedly linked to the relationship between income (collections) / expenses (payments). An imbalance in the cash generated leads to solvency or equity problems and, without a doubt, problems in cash management.

The third dimension selected and previously disclosed by de Andres-Alonso et al. (2016) is leverage. In this dimension, what is measured is the ability of the organization to meet the payment of its debts as they become due, and it does so by measuring the ratio of total assets to debt. Other authors had already taken this variable into consideration, as they studied technical insolvency or the risk of insolvency (Keating et al., 2005 and Gordon et al., 2013).

We propose to measure this dimension with the following ratios: distance to bankruptcy and leverage.

The fourth dimension selected is liquidity (from Andres-Alonso et al., 2016). This dimension analyses the capacity of the entity to meet its liabilities in the short term. Liquidity tensions arise from cash flow imbalances, occurring from the relationship that exists between income and the amount received, as well as from expenses and what is paid. The interest of analysing this dimension in non-profit entities in a situation of vulnerability comes from the ability of the entity to reduce its assets (whether current or non-current assets) when its income is insufficient.

These last two dimensions, leverage and liquidity, are related to the entity's ability to meet payments. If the entity has a healthy financial situation, that is, low debts and a high financial balance, the entity could deal with payment problems over several years perhaps. On the other hand, it must also be taken into account that there are entities that get used to living with high debt rates. For this reason, it is necessary, when carrying out an analysis, to take into account the different aspects of financial vulnerability because if we only consider one aspect, we may wrongly perceive the financial reality of the entity.

The last dimension is reputation, the reputation of the entity in society is a leading element. The image that the entity portrays will establish a reputation within society and that reputation will determine the collaboration it receives (either by number of volunteers or financial aid in the form of donations). In fact, the study by Harvey & McCrohan (1988) revealed that donors are more willing to contribute to organizations that spend 60 percent or more of their resources on programmes (Ryan & Irvine, 2012). In general, CSR has a positive impact on reputation and investment in CSR has a direct effect on an entity’s image.

The possibility of imbalance in each of the previous variables can be supplemented by rapidly obtaining resources supported by the prestige of the entity, by its ability to go to the NPOs capital market: recruiting volunteers and collecting donations, both public and especially private. However, it should be taken into consideration that the concept of image and reputation, concepts that are interrelated but can be differentiated (Gotsi & Wilson, 2001), are used to define a large number of things or phenomena (Capriotti, 2009). This polysemy results in the difficulty of concentrating its meaning and much more its valuation. Reputation can be a corporate management tool that acts on stakeholders; while image performs more on the general public (Capriotti, P., & Losada, 2007). Furthermore, when speaking of a possible mental perception of the receiver or a desired perception managed by the issuer, we are faced with a concept that is found in both spheres - receiver and issuer - within a normal communication process. In short, we must appreciate that, but with certain nuances with profit-making entities, NPOs are more exposed to social judgment as they base their activities on the trust of their partners / volunteers who seek to support their cause or objectives. For this reason, an image of loyalty and trust is of great importance and should be supported by adequate transparency. Agency problems derive from the fact that the benefactors (main) are related to the recipients through management (agents).

In this sense, from the scope of our study and the capacity to manage financial vulnerability, the issuer's approach may be more interesting, as it refers to the image or the set of elements that the organization wants its public to target or associate with the entity. We speak of a desired perception, as a created product that must be adequately transmitted (Capriotti, 2009). It is evident that a weak product, poorly defined in terms of image and poorly communicated, will lead to deficiencies in attracting resources and volunteering, which in the long run may cause problems in its net assets or in its lack of liquidity, among other aspects. Through this approach, we subtly indicate that image is one more net asset, but it is impossible to quantify with precision due to its internal generation.

However, in our analysis, we must not forget the role of the receiver, where misinformation or badly interpreted information received from the entity has negative consequences and once communicated are less controllable by the organization. In either case, failure in the communication process, without a pre-existing reputational issue, can limit the sourcing of resources and volunteers. Therefore, this aspect must be measured with special care. In short, the scope of the reputational dimension must take into account the development of a series of typical dimensions used for institutional activity: reality, identity, communication and image (Cháves, 1998).

At this point, it is important to point out that quantifying reputation in the form of an indicator implies summarizing data with precision, such as the variation in volunteering and/or the amount of donations received. Both variables need to consider the relevance of the environment and the economic situation which are sometimes confronted. In a worst-case scenario, it will be more difficult to receive contributions, but possibly easier to attract volunteers; in a better case scenario, a decrease in volunteering is possible due to a lower availability of free human resources, fewer objectives to be achieved, but greater potential to receive resources.

Specifically, we propose the two variables below to measure reputation:

– Number and quantity of donations received (average variation of donations over several years) and,

– Number of volunteers, total or average during the year and its temporal variation over several exercises. We also propose more homogeneous policies on information relating to volunteers on a global basis.

By using both types of indicators, we incorporate the dual perspective, both that of the receiver and that of the issuer of the NPO's image / reputation, which is reflected in quantifiable objective data.

Figure. 1. Pentagram including 5 dimensions for detecting the financial vulnerability of non-profit entities

Source: Own elaboration

6. Conclusions

The entities that form part of the social economy and are known as NPOs were created to respond to social needs. However, many of these entities close each year, after a period of financial difficulty, regardless of whether they achieve their corporate objectives or not. Given their importance at a social and economic level, the study of their financial vulnerability is an area of special interest, not only to highlight the factors that characterize these entities in financial difficulty but also to develop mechanisms to anticipate future undesirable situations and to avoid financial failure as a consequence.

In this way, the entity itself could incorporate the necessary changes in its structure and its management to redirect the situation. In our study, after a detailed analysis of previous academic literature that examines this said vulnerability, we construct a pentagram representing the five dimensions - some interrelated - or elements that must be taken into consideration in their vulnerability study, namely, performance, operational dimension, leverage, liquidity and, above all, reputation.

In the area of performance, we are in the area of economic resource management when measuring the input - output relationship of this type of organizations processes. Relevance is given to the quantification of the price and value of the input and in the number of processes or services derived from the organisation’s activity. In the operating area, we examine equity, the relationship between income and expenses and the effect they may have on the net assets structure of the entity. A logical weakening in its structure could raise doubts about its continued management and survival.

In relation to the said situation of the entity's resources or solvency, its leverage or its ability to meet third party obligations, together with its liquidity, delimits the two most relevant areas from the balance sheet point of view and also the liquidity status of the entity. It presents a static photograph of equity that must be accompanied by a dynamic vision in a limited time horizon.

Finally, the dimension that acts as an umbrella for the model is an NPO's reputation and image, represented by a corporate communication process from the entity itself through the appropriate channel and its perception by the recipient. Although it has its inherent reflection in the recruitment of resources and the variation in the number of volunteers, it must be appreciated that the said evolution of the entity does not necessarily have to be justified by the existence of reputational damage derived from dubious actions. It may also be due to the fact that the product to be communicated is not adequately defined or because of a weakness in the message and the channel used, causing negative effects on a limited reputational aesthetics. In addition, the current situation of the economic environment is also relevant when considering its effect on these two variables - income and volunteering -. With a positive economic environment, there is greater capacity to attract resources, but a lower level of volunteering; While, in the face of a bad economic situation, in which the NPO will have more need to fulfil its objectives, it will probably have a greater number of volunteers but the capacity to attract both public and private resources will be more limited.

In short, this model establishes a necessary theoretical framework that covers the dispersion of criteria in the definition of financial vulnerability. This will allow the construction of applied studies on the evolution and situation of the third sector, justifying pre-existing data and reaching a study on its future evolution. Future research can develop a mechanism for calculating financial vulnerability based on the five dimensions analysed and proposed in this study. The objective is to offer a guide to continually assess the possible vulnerability of the entity, the results of which could provide alerts to focus on needed areas of management and thus avoid a future undesirable entity failure. More research is necessary on the management and inormation transparency function in NPOs to detect financial vulnerability at an early stage.

Conflicts of Interest: The authors declare no conflicts of interest.

Author Contribution: Inmaculada García Jimeno, Anne Marie Garvey, Carlos Mir and Rocio Flores Jimeno contributed to the Conceptualization of Ideas, Formal analysis, Investigation, Methodology, Writing original draft. Inmaculada García Jimeno & Anne Marie Garvey contributed to the Data curation, Funding acquisition, Project administration, Resources, Software, Supervision, Validation, Visualization and Reviewing and Editing the final version.

Funding: The authors are grateful for the support by the Spanish Ministry of Science, Innovation and Universities for projects PID2019-105570GB-I00, CCG19/CCJJ-042, PID2020-114563GB-I00 and projects from Alcala University CM/JIM/2019-044, UAH/EV1180 and UAH/EV1090.

7. References

Abraham, A. (2003). Financial sustainability and accountability: a model for nonprofit organisations. AFAANZ 2003 Conferenc e Proceedings, 6-8 July 2003.

Adrián, T., Boyarchenko, N., & Giannone, D. (2019). Vulnerable growth. American Economic Review, vol. 109, Nº 4, pp. 1263 - 89. DOI: 10.1257/aer.20161923.

AECA. (2010). Los Estados Financieros de las Entidades Sin Ánimo de Lucro. AECA, (Documento 2).

AECA. (2012). Indicadores para entidades sin fines lucrativos. Comisión de Entidades Sin Fines Lucrativos de AECA, Documento 3.

Aguado Muñoz, R.; Retolaza Ávalos, J.L.; Alcañiz González, L. (2021). Social accounting in organizations of the Social Economy: The ARTE program applied to the CLADE Group. REVESCO. Revista de Estudios Cooperativos, vol. 138, e73865. https://dx.doi.org/10.5209/reve.73865.

Altman, E., Iwanicz-Drozdowska, M., Laitinen, E., & Suvas, A. (2015). Financial and non-financial variables as long-horizon predictors of bankruptcy. Available at SSRN 2669668. http://dx.doi.org/10.2139/ssrn.2669668.

Altman, E. I. (1968). Financial Ratios, Discriminant Analysis and the Prediction of Corporate Bankruptcy. The Journal of Finance, vol. 23, Nº 4, pp. 589–609. http://www.jstor.org/stable/2978933/ https://doi.org/10.2307/2978933.

Andersen, P., & Petersen, N. C. (1993). A procedure for ranking efficient units in data envelopment analysis. Management Science, vol. 39, Nº 10, pp. 1261–1264. https://doi.org/10.1287/mnsc.39.10.1261.

Argenti, J. (1976). Corporate Collapse the causes and symptoms. In John Wiley and Sons (Ed.), Theory of Reliability and Life Testing: Probability models. ProQuest Central pg.

Arnau, A., Fuertes Iluminada, & Maset-Llaudes, A. (2007). El Tercer Sector en la Comunidad Valenciana: El Caso de las Fundaciones Autores. AECA, pp. 47.

Arturo Grosso Rincón, C. (2013). La economía social desde tres perspectivas: tercer sector, organizaciones no gubernamentales y entidades sin ánimo de lucro, vol. 18, Nº 1, pp. 143-158.

Ashley, S., & Faulk, L. (2010). Nonprofit competition in the grants marketplace: Exploring the relationship between nonprofit financial ratios and grant amount. Nonprofit Management and Leadership, vol. 21, Nº 1, pp. 43-57. https://doi.org/10.1002/nml.20011.

Balcaen, S., & Ooghe, H. (2006). 35 years of studies on business failure: An overview of the classic statistical methodologies and their related problems. In British Accounting Review, vol. 38, Nº 1, pp. 63-93. https://doi.org/10.1016/j.bar.2005.09.001.

Barahona, J. H., Pérez, V. M., & Cruz, N. M. (2009). Implications of internal organization on efficiency. The use of agency theory and DEA methodology to Spanish NGDOs. Cuadernos de Economía y Dirección de La Empresa, Nº 40, pp.17-46. https://doi.org/10.1016/S1138-5758(09)70041-6.

Bellostas, A. J., Brusca, I., & Moneva, J. M. (2006). Usefulness of non-profit private entities financial reporting for management purposes [Utilidad de la información financiera para la gestión de las entidades privadas no lucrativas]. Revista de Contabilidad, vol. 9, Nº 18, pp. 87–109.

Bhattacharya, R., & Tinkelman, D. (2009). How tough are better business bureau/wise giving alliance financial standards? Nonprofit and Voluntary Sector Quarterly, vol. 38, Nº 3, pp. 467-489. https://doi.org/10.1177/0899764008316120.

Bowman, H. W., Keating, E. K., & Hager, M. (2005). Organizational slack in nonprofits. In Annual Meeting of the Academy of Management, Honolulu, HI. Retrieved from http://mhager.net.

Bowman, W. (2011). Financial capacity and sustainability of ordinary nonprofits. Nonprofit Management and Leadership, vol. 22, Nº 1, pp. 37–51. https://doi.org/10.1002/nml.20039.

Burger, R. (2012). Reconsidering the Case for Enhancing Accountability Via Regulation. Voluntas, vol. 23, Nº 1, pp. 85–108. https://doi.org/10.1007/s11266-011-9238-9.

Capriotti, P., & Losada, J. (2007). Imagen, posicionamiento y reputación: similitudes y diferencias conceptuales. In Colección Libros de la Empresa, pp. 83-103.

Capriotti, P. (2009). De La Imagen a la Reputación. Análisis de Similitudes y Diferencias. Razón y Palabra, Nº 70, pp. 1–10. http://www.razonypalabra.org.mx.

Carroll, D. A., & Stater, K. J. (2009). Revenue diversification in nonprofit organizations: Does it lead to financial stability? Journal of Public Administration Research and Theory, vol. 19, Nº 4, pp. 947-966. https://doi.org/10.1093/jopart/mun025.

Carvalho, A.O., Rodrigues, L.L. & Branco, M.C. (2017) Factors influencing voluntary disclosure in the annual reports of Portuguese foundations, Voluntas, vol. 28, Nº 5, pp. 2278-2311, DOI: 10.1007/s11266-017-9883-8.

Chang, C. F., & Tuckman, H. P. (1994). Revenue diversification among non-profits. VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations, vol. 5, Nº 3, pp. 273–290.

Charnes, A., Cooper, W. W., Lewin, A. Y., & Seiford, L. M. (1997). Data envelopment analysis: Theory, methodology, and applications. Journal of the Operational Research society, vol. 48, Nº 3, pp. 332-333. New York, NY: Springer Science & Business Media. https://doi.org/10.1057/palgrave.jors.2600342.

Cháves, N. (1998). Diseño industrial y posicionamiento corporativo. Economía Industrial, Nº 324, pp. 33–36.

Cnaan, R. A., Jones, K., Dickin, A., & Salomon, M. (2011). Nonprofit Watchdogs Do They Serve the Average Donor? Nonprofit Management and Leadership, vol. 21, Nº 4, pp. 381-397. https://doi.org/10.1002/nml.20032.

Comyns, B., & Franklin-Johnson, E. (2018). Corporate Reputation and Collective Crises: A Theoretical Development Using the Case of Rana Plaza. Journal of Business Ethics, vol. 150, Nº 1, pp. 159-183. https://doi.org/10.1007/s10551-016-3160-4.

Cordery, C. J., Sim, D., & Baskerville, R. F. (2013). Three models, one goal: Assessing financial vulnerability in New Zealand amateur sports clubs. Sport Management Review, vol. 16, Nº 2, pp. 186–199. https://doi.org/10.1016/j.smr.2012.08.002.

Corral-Lage, & Peña-Miguel. (2016). La necesidad de un modelo propio de indicadores para las entidades no lucrativas españolas: indicadores de organización y dirección. Revista Internacional de Economía y Gestión de las Organizaciones, 2014, vol. 3, Nº 2. https://doi.org/10.37467/revgestion.v3i2.1158.

Corral Lage, J., & Elechiguerra Arrizabalaga, C. (2014). Razones por las que se demanda una necesidad de transparencia en las entidades no lucrativas: estudio empírico. Harvard Deusto Business Research, vol. 3, Nº 1, pp. 47–61. https://doi.org/10.3926/hdbr.38.

Coupet, J., & Berrett, J. L. (2019). Toward a valid approach to nonprofit efficiency measurement. Nonprofit Management and Leadership, vol. 29, Nº 3, pp. 299-320. https://doi.org/10.1002/nml.21336.

De Andres-Alonso, P., Garcia-Rodriguez, I., & Romero-Merino, M. E. (2016). Disentangling the Financial Vulnerability of Nonprofits. Voluntas, vol. 27, Nº 6, pp. 2539–2560. https://doi.org/10.1007/s11266-016-9764-6.

De Andrés-Alonso, P., Garcia-Rodriguez, I., & Romero-Merino, M. E. (2015). The Dangers of Assessing the Financial Vulnerability of Nonprofits Using Traditional Measures: The Case of the Nongovernmental Development Organizations in the United Kingdom. Nonprofit Management and Leadership, vol. 25, Nº 4, pp. 371-382. https://doi.org/10.1002/nml.21134.

Elbers, W., & Arts, B. (2011). Keeping body and soul together: Southern NGOs’ strategic responses to donor constraints. International Review of Administrative Sciences, vol. 77, Nº 4, pp. 713–732. https://doi.org/10.1177/0020852311419388.

Fernandez, J. J. (2008). Causes of dissolution among Spanish nonprofit associations. Nonprofit and Voluntary Sector Quarterly, vol. 37, Nº 1, pp. 113-137. https://doi.org/10.1177/0899764006298965.

Fischer, R. L., Wilsker, A., & Young, D. R. (2011). Exploring the revenue mix of nonprofit organizations: Does it relate to publicness? Nonprofit and Voluntary Sector Quarterly, vol. 40, Nº 4, pp. 662–681. https://doi.org/10.1177/0899764010363921.

Flores-Jimeno, R., & Jimeno-García, I. (2019). Analysing business failure processes. International Journal of Accounting and Finance, vol. 9, Nº (2–4), pp. 130–151. https://doi.org/https://doi.org/10.1504/IJAF.2019.106754.

Flores-Jimeno, R., & Jimeno-García, I. (2017). Dynamic analysis of different business failure process. Problems and Perspectives in Management, vol. 15, Nº (2–3), pp. 486–499. https://doi.org/10.21511/ppm.15(si).2017.02.

Froelich, K. A. (1999). Diversification of Revenue Strategies: Evolving Resource Dependence in Nonprofit Organizations. Nonprofit and Voluntary Sector Quarterly, vol. 28, Nº 3, pp. 246–268. https://doi.org/10.1177/0899764099283002.

Frumkin, P. & Keating, E.K. (2011). Diversification reconsidered: The risks and rewards of revenue concentration, Journal of Social Entrepreneurship, vol. 2, Nº 2, pp. 151-164. https://doi.org/10.1080/19420676.2011.614630.

García Rodríguez, I. (2017). Gobierno y vulnerabilidad financiera de las entidades no lucrativas: un análisis de las INGDs de España y Reino Unido. Universidad de Burgos.

Gazengel, A. & Thomas, P. (1992). Les défaillances d’entreprises. Les Cahiers de recherche- ESCP. Série Economie et finance.

Gent, S. E., Crescenzi, M. J. C., Menninga, E. J., & Reid, L. (2015). The reputation trap of NGO accountability. International Theory, vol. 7, Nº 3, pp. 426–463. https://doi.org/10.1017/S1752971915000159.

Gilbert, L., Menon, K., & Schwartz, K. (1990). Predicting bankruptcy for firms in financial vulnerability. Journal of Business Finance and Accounting, vol. 17, Nº 1, pp. 161–171. https://doi.org/10.1111/j.1468-5957.1990.tb00555.x.

Giner, B., & Gill de Albornoz, B. (2013). Predicción del fracaso empresarial en los sectores de construcción e inmobiliario: Modelos generales versus específicos. Universia Business Review, Nº 39, pp. 118–131. https://dialnet.unirioja.es/servlet/articulo?codigo=4392078.

Golden, L. L., Brockett, P. L., Betak, J. F., Smith, K. H., & Cooper, W. W. (2012). Efficiency metrics for nonprofit marketing/fundraising and service provision-a DEA analysis. Journal of Management and Marketing Research, vol. 10, Nº 1, pp. 1–25.

González, M., & Rúa, E. (2007). Análisis de la eficiencia en la gestión de las fundaciones: una propuesta metodológica. CIRIEC-España, Revista de Economía Pública, Social y Cooperativa, Nº 57, pp. 117–149.

González Quintana, M. J. (2003). El modelo de información contable en las entidades privadas sin ánimo de lucro: una propuesta de mejora para las asociaciones. Universidad de Málaga. http://hdl.handle.net/10630/2542.

Gotsi, M., & Wilson, A. M. (2001). Corporate reputation: Seeking a definition. In Corporate Communications: An International Journal, Vol. 6, Nº 1, pp. 24–30. https://doi.org/10.1108/13563280110381189.

Green, E., Ritchie, F., Bradley, P., & Parry, G. (2021). Financial resilience, income dependence and organisational survival in UK charities. VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations, vol. 32, Nº 5, pp. 992-1008. https://doi.org/10.1007/s11266-020-00311-9.

Greenlee, J. S., & Trussel, J. M. (2000). Predicting the financial vulnerability of charitable organizations. Nonprofit Management and Leadership, vol. 11, Nº 2, pp. 199-210. https://doi.org/10.1002/nml.11205.

Greenlee, J., & Trussel, J. M. (2004). A Financial Rating System for Charitable Nonprofit Organizations. Research in Government and Nonprofit Accounting, vol. 11, pp. 105–128.

Hager, M.A. (2001): Financial vulnerability among arts organizations: A test of the Tuckman Chang measures, Nonprofit and Voluntary Sector Quarterly, vol. 30, Nº 2, pp. 376-392. https://doi.org/10.1177/0899764001302010.

Harvey, J. W., & McCrohan, K. F. (1988). Fundraising Costs-Societal Implications For Philanthropies. Business and Society; Spring, vol. 27, Nº 1, pp. 15-22. https://doi.org/10.1177/000765038802700103.

Helmig, B., Ingerfurth, S., & Pinz, A. (2013). Success and Failure of Nonprofit Organizations: Theoretical Foundations, Empirical Evidence, and Future Research. VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations, vol. 25, no 6, p. 1509-1538. https://doi.org/10.1007/s11266-013-9402-5.

Hernangómez Barahona, J., Martín Pérez, V., & Martín Cruz, N. (2008). Implicaciones de la organización interna sobre la eficiencia. La aplicación de la teoría de la agencia y la metodología DEA a las ONGD españolas* Implications of Internal Organization on Efficiency. The Use of Agency Theory and DEA Methodology to Spanish. Cuadernos de Economia y Direccion de La Empresa, vol. 12, Nº 40, pp. 17-46. https://doi.org/10.1016/S1138-5758(09)70041-6.

Hodge, M. M., & Piccolo, R. F. (2005). Funding Source, Board Involvement Techniques, and Financial Vulnerability in Nonprofit Organizations: A Test of Resource Dependence. Nonprofit management and leadership, vol. 16, Nº 2, pp. 171-190. https://doi.org/10.1002/nml.99.

Hofmann, M. A., & McSwain, D. (2013). Financial disclosure management in the nonprofit sector: A framework for past and future research. Journal of Accounting Literature. https://doi.org/10.1016/j.acclit.2013.10.003.