![]() ISSN: 1885-8031

ISSN: 1885-8031

https://dx.doi.org/10.5209/REVE.91314

Nueva metodología secuencial para diseñar, probar y escalar Modelos de Negocio Sostenibles

Vanessa Campos Climent[1]![]() ,

Joan Ramon Sanchis Palacio[2]

,

Joan Ramon Sanchis Palacio[2]![]() y Ana Teresa Ejarque Catalá[3]

y Ana Teresa Ejarque Catalá[3]![]()

Recibido: 23 de febrero de 2023 / Aceptado: 17 de julio de 2023 / Publicado: 6 de octubre de 2023

Resumen. En la actualidad, la agenda 2030 ha puesto las preocupaciones sociales y ambientales en el centro de la práctica empresarial. Esto ha impulsado a los nuevos emprendimientos a integrarlos a su modelo de negocio desde sus primeras etapas de desarrollo. Así, muchos de los comportamientos tradicionalmente asociados con las empresas sociales están siendo adoptados por las empresas ordinarias. Este proceso se menciona en la literatura como hibridación. En consecuencia, este enfoque híbrido sostenible adoptado por una cantidad cada vez mayor de nuevas empresas requiere el desarrollo de nuevas herramientas para diseñar, probar y escalar modelos de negocios sostenibles que aborden la integración de las preocupaciones sociales y ambientales en su modelo de negocios desde sus etapas iniciales de desarrollo. Sin embargo, hasta la fecha, no existe una herramienta disponible totalmente capaz de diseñar, probar y escalar modelos de negocios sostenibles.

Por lo tanto, el presente trabajo tiene como objetivo llenar este vacío en la literatura proporcionando una metodología secuencial que combina el marco de la Economía del Bien Común, el Lean Start-up y el método Delphi. Los autores han desarrollado la metodología docente propuesta en este artículo durante cinco años consecutivos, utilizando la investigación basada en la acción con estudiantes internacionales y locales del Curso de Emprendimiento que se imparte en el Grado en Administración y Dirección de Empresas de la Universitat de València.

Palabras clave: Metodología de aprendizaje en emprendimiento; Investigación basada en la acción; Innovación sostenible; Economía del Bien Común; Lean Start-up; Método Delphi.

Claves Econlit: L26; M14; O35.

[en] Presenting a new sequential methodology to design, test, and scale Sustainable Business Models

Abstract. These days the 2030 agenda has put social and environmental concerns at the core of business practice. This has driven new ventures to integrate them into their business model since their first stages of development. Thus, many of the behaviors traditionally associated with social enterprises are being adopted by ordinary businesses. This process is mentioned in the literature as hybridization. Consequently, this sustainable hybrid approach adopted by a growing amount of new ventures requires the development of new tools to design, test, and scale sustainable business models addressing the integration of social and environmental concerns into their business model since their initial stages of development. However, up to date, there is no tool fully capable of designing, testing, and scaling sustainable business models.

Thus, the present work is aimed at filling this gap in the literature by providing a sequential methodology that combines the Economy for the Common Good framework, the Lean Start-up, and the Delphi method. The authors have developed the teaching methodology proposed in this paper over five consecutive years, using Action-based research with international and local students of the Entrepreneurship Course delivered at the Degree in Business Administration of the University of València.

Keywords: Entrepreneurship teaching methodology; Action-based research; Sustainable Innovation; Economy for the Common Good; Lean Start-up; Delphi method.

Summary. 1. Introduction. 2. Overcoming the traditional wisdom of value creation since starting the business. 3. Why test and scale SBM using the Lean Start-up method. 4. Full design of a scalable Sustainable Business Model using the Tripple Layered Business Model Canvas. 5. Conclusions. 6. References.

How to cite. Campos Climent, V.; Sanchis Palacio, J.R. & Ejarque Catalá, A.T. (2023). Presenting a new sequential methodology to design, test, and scale Sustainable Business Models. REVESCO. Revista de Estudios Cooperativos, 1(145), e91314. https://dx.doi.org/10.5209/reve.91314.

The success of an entrepreneurial project highly relies on its business model. The concept of a business model (BM) emerged for the first time in the mid-20th Century as a “theory of a business” (Drucker, 1955). Despite scholars do not fully agree on its definition, the most accepted definition of BM is “the rationale of how an organization creates, delivers and captures value” (Osterwalder & Pigneur, 2010: 14).

Thus, the underlying key variables of the above-mentioned definition are the type of value that an organization can create and deliver, and the stakeholders to whom this value creation is addressed. Likewise, Osterwalder & Pigneur (2010) created the business model canvas (BMC), a tool for supporting the business model design process. However, such BMC only considered economic value as the only source of value to be created and delivered by organizations (Osterwalder et al., 2005; Falle et al., 2016).

In the last twenty years, organizations have experienced rising social pressure to respond to sustainability concerns (Dyllick & Hockerts, 2002; Johnson & Schaltegger, 2016; Engert et al., 2016; Pinelli & Maiolini, 2017). This drives us to the concept of entrepreneurship for sustainable development or sustainable entrepreneurship as a multilevel phenomenon that connects social, environmental, and economic dimensions (Johnson & Schaltegger, 2020; Meseguer-Sánchez et al., 2021; Moya-Clemente et al., 2021). In this sense, some authors advocate exploring new ways of sustainability-oriented business model innovation (Schaltegger et al., 2011; Schaltegger & Wagner, 2011; Trimi & Berbegal-Mirabent, 2012), creating the triple-layered business model canvas (TLBMC) (Joyce & Paquin, 2016). To do so, they followed a triple-bottom-line approach to organizational sustainability (Elkington, 1994; Elkington, 2004; Schaltegger, 2014; Schaltegger et al., 2016; Schaltegger et al., 2018; Birkin et al., 2019).

Yet, BMC and TLBMC are not exempt from criticism. Indeed, over the last few years, some authors have stressed that both tools are based on a series of untested hypotheses, and this is what explains the high rates of failure among start-ups. That is why, lean start-up (LSU) techniques are developed to avoid setting up business models that rarely survive contact with customers and other key stakeholders (Stubbs & Cocklin, 2008; Schaltegger & Lüdeke-Freund, 2011; Blank, 2013; Hörisch et al., 2014). Thus, LSU techniques constitute what is known as the “getting out of the building” techniques whilst BMC and TLBMC are known as “on the desk” techniques (Figge et al., 2002; Bocken & Snihur, 2020).

Despite this, in the literature body, LSU techniques are not used to test the underlying hypotheses following a sustainability approach (Sanchis, Campos & Ejarque, 2020). Therefore, in our view, the current situation requires a new holistic teaching methodology to be developed to address the current challenges in the Entrepreneurship field.

On the other hand, the Economy for the Common Good (ECG) framework as a sustainable organizational model enables the embedding of social and environmental concerns into business operations (Felber, 2010; Dyllick & Muff, 2016; Felber, Campos & Sanchis, 2019). Hence, some authors point to the ECG framework as an organizational model that allows the integration of the SDGs into micro small, and medium-sized enterprises' business models, being one of the ECG contributions its metrics that can facilitate the hypotheses testing (Ejarque & Campos, 2020; Campos, Sanchis & Ejarque, 2020). We argue that the combination of the above-mentioned methodologies, used sequentially, can drive to overcome the limitations they show when used separately.

Taking these antecedents into account, the present work has the following objectives: 1) Provide a combined teaching methodology based on the ECG framework that enables the embedding of sustainability concerns into the BM; 2) Provide a combined teaching methodology based on LSU and the Delphi method as a prospective technique to test the core assumptions and hypotheses made to generate the initial Sustainable Business Model (SBM); 3) Describe how to pivot the SBM using the LSU and the results of the Delphi method used to test the hypothesis and core assumptions; and 4) Scale and design the full SBM using the TLBMC taking the hypothesis testing based on LSU and the Delphi method as a base.

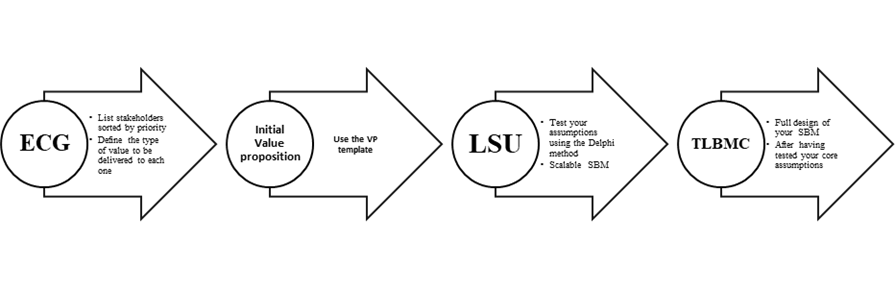

To do so, we propose a sequential data-driven process to design, test, and scale SBM based on the ECG framework, the LSU, the Delphi method, and the TLBMC. Figure 1 below depicts the sequential process.

Figure. 1. The sequential process to design, test, and scale SBM.

Source: own elaboration

It is worth mentioning that we have been developing this new teaching methodology for over five consecutive years in the Entrepreneurship courses we taught at the Degree in Business Administration of the University of València with international and local students (Betáková et al., 2020). In these Entrepreneurship courses, we employ project-based learning (PBL). Thus, we relied on the following principles of action research (Somekh, 2005): (1) the combination of research and action; (2) the collaborative partnership of researchers and participants (the students enrolled in our courses); (3) the development of knowledge and understanding of a particular case (the process of designing, testing and scaling SBM); (4) vision on social transformation and personal engagement; and (5) evoking learning for participants through combining research, actions, and reflection of the practice.

To monitor the developing process of the new teaching methodology we used multiple sources of information. Namely, we refer to reflections made by students before the beginning of the courses in pre-start meetings with instructors, instructors’ participative observations during the courses, and instructors’ notes in their teaching diaries.

Finally, the present work is structured into five sections. Following the present introduction, we find section two which proposes a process to overcome the traditional wisdom of value creation using the Economy for the Common Good (ECG) framework. Thereafter, section three depicts how to adapt the Lean Start-up method to test SBM core assumptions and hypotheses using a prospective technique (Delphi method). Section four completes the process by depicting the full SBM design based on the results of the LSU testing using the Delphi method. Finally, section 5 summarizes the conclusions including an overview of the sequential process we propose in this paper.

2. Overcoming the traditional wisdom of value creation since starting the business

In the present times, several authors advocate for redefining and reorienting the concept of value creation using stakeholder theory as a reference (Carroll, 1991; Porter & Kramer, 2011; Figge et al., 2002; Busch et al., 2018). Thus, following stakeholder theory (Freeman, 1984; Freeman et al., 2004; Freeman, 2008; Parmar et al., 2010), a firm is called to create value, including social and environmental value, for all its stakeholders to succeed (Klewitz & Hansen, 2014; Murillo, 2022).

Hence, Donaldson & Walsh (2015) point out what they call “collective value” as the goal of businesses. Likewise, they define collective value as “the agglomeration of the Business Participants’ Benefits […] net of any aversive Business outcome” (Donaldson & Walsh, 2015: 188). Such a definition involves the stakeholders’ role awareness and the recognition of possible positive and negative impacts of business operations.

In light of the abovementioned considerations, Busch, et al., (2018) propose a massive system change toward economic, societal, and sustainability transition to happen in three phases whose definition is based on providing the answers to three key questions: (1) Who matters for value creation?; (2) How can financial value be generated in a stakeholder context?; and (3) How to transform business models?.

Thereafter, the phases are defined as follows. In Phase I, Busch et al. (2018) propose to complete a strategic reorientation by enlightening value maximization. This is expected to happen when organizations create as much value for all stakeholders as possible and when they are driven to Long-term value maximization for which stakeholders and their interests matter. i. e. Value creation should be centered on stakeholders, not only on shareholders. For this reason, our proposal to design and scale SBM takes stakeholders as the starting point and begins by identifying the key stakeholders to whom the organization addresses its value creation.

In Phase II, Busch et al. (2018) respond to the performance debate by advocating for Sustainable Value Creation. According to them, organizations create value by addressing societal needs and sustainability (environmental) challenges. Thus, according to them, the value creation process begins when organizations address social and environmental concerns, and later turn them into business opportunities (Zahra et al., 2009). Consequently, we propose that the SBM design should consider first social and environmental value creation.

Finally, in Phase III, Busch et al. (2018) call for the metamorphosis of businesses to happen based on collective value creation. Thus, they argue that organizations should maximize collective value and be accountable to all stakeholders (future, present, and past). This way, embedding social and environmental concerns becomes a guiding principle in the value-creation process (Murillo, 2022). As a consequence, this changes the way of doing business.

In line with the process depicted by Busch et al. (2018), we propose to take the Common Good Matrix (CGM) as the starting point to design SBM (Sanchis & Campos, 2019; Felber, Campos & Sanchis, 2019). The CGM is a business management tool designed to embed sustainability into ordinary business operations. This tool is part of the Economy for the Common Good (ECG) model (Felber, 2010). In this sense, Campos (2016: 13) based on how civil society can influence the decision-making process that occurs within the organizational boundaries, classifies the ECG model as an alternative model of enterprise that allows civil society to influence the business-making-decisions process and set up a different way of doing business. In her conclusions, she provides a comparison between three different models of alternative enterprises: social economics businesses, B corporations, and ECG businesses. Hence, whilst in traditional social economics business influence in the decision-making process occurs as a consequence of membership that is spread among civil society and associated with some specific social economy legal forms. In B Corporations and ECG businesses, civil society influences the decision-making process through the stakeholders' theory (Freeman, 1984), i.e. membership is not a first-order condition to have a significant influence in the decision-making process. Consequently, B Corporations and ECG businesses base their management practices on the management of their relationships with internal and external stakeholders to embed sustainability into their strategies and are not restricted to any legal form. In conclusion, whilst from a traditional viewpoint, social economy organizations use membership and some specific legal forms to facilitate the influence of civil society in the decision-making process embedding social and environmental values as an essential part of business operation. In contrast, B Corporations and ECG businesses operate completely under the premise that civil society as a key stakeholder can influence the organizational decision-making process to embed social and environmental values into ordinary business operations.

Thus, the CGM is the tool that guides the initial steps of the SBM design process. It is conceived as a strategic matrix to guide the integration of sustainability and social concerns into the business operation. To do so, the CGM takes the organization’s relationship with its stakeholders as a reference and, drives it according to four cross-values: human dignity, solidarity and social justice, environmental sustainability, and, transparency and co-determination. In addition, some authors (Giesenbauer & Müller-Christ, 2018) have associated the different cells and indicators of the CGM with the SDGs holding (Sachs, 2012) that the ECG model is an effective framework to integrate the SDGs into the business operation. Hence, we argue that taking the CGM as the starting point in the design of SBM allows us to embed the SDGs from scratch in the design of SBM. Consequently, aligning the organizational purpose with social and environmental concerns.

Associated with the CGM, the Economy for the Common Good (ECG) framework proposes a set of indicators to monitor the process evolution that constitutes the ECG measurement theory. On its side, the Common Good Balance Sheet (CGBS) takes such a set of indicators as a starting point and, works as an integrated report that allows process monitoring. The main novelty of the CGBS as an integrated report, however, is that it works as a source of information related to sustainability concerns for both internal and external stakeholders (Felber, Campos & Sanchis, 2019; Ejarque & Campos, 2020).

As an antecedent of the CGM, it is worth mentioning that Ketola, (2010) had also proposed the idea of employing a strategic matrix to support the embedding of social and environmental concerns in the business context, i.e. the Corporate Responsibility Portfolio Matrix. However, such a matrix did not work together with any type of integrated report.

Figure 2 below shows the CGM version 5.0. Its rows depict the five groups of stakeholders and, its columns specify the cross-values that drive the organization's relationship with its stakeholders. On its cells, we find the different sources of value creation associated with every specific stakeholder group and the specific SDG it contributes to addressing. Thus, linking stakeholders' value creation with social and environmental matters and SDGs.

Figure. 2. The Common Good Matrix (CGM).

Source: https://www.ecogood.org/apply-ecg/sustainable-development-goals/

Because of the scarcity of resources and capabilities, it is not realistic for a new venture to design a SBM aimed at creating all the types of value mentioned above for all its stakeholders (Dean & McMullen, 2007; Guzmán & Trujillo, 2008). For this reason, we propose to base the SBM on the CGM but prioritize the stakeholders and the values according to the possibilities of the start-up. To this end, we designed Table 1 below and named it the priority matrix. Such a priority matrix is conceived to set up the organization’s priorities in terms of stakeholders and social and environmental values to be created for every stakeholder group. It is worth mentioning that it is not expected that a start-up creates a whole range of social and environmental values for every one of its stakeholders.

Table. 1. The priority matrix.

|

|

Key Stakeholder 1 |

Key Stakeholder 2 |

Key Stakeholder 3 |

Key Stakeholder 4 |

|

Cross-value 1 |

|

|

|

|

|

Cross-value 2 |

|

|

|

|

|

Cross-value 3 |

|

|

|

|

|

Cross-value 4 |

|

|

|

|

Source: own elaboration

Thus, the top row of the priority matrix should provide a brief portrait (i.e., including their main traits) of every specific stakeholder for whom we aim to create value, sorted by degree of prioritization for the start-up. The column on the left should provide the list of values (social and environmental) to be created sorted by degree of prioritization for the start-up. As a result, every cell of the table will contain the answer that the start-up can provide to its key stakeholders in terms of social and environmental concerns given the start-up priorities. Therefore, providing specific responses to the question “What can I do for you?”. It is worth mentioning that, at this stage, the answers provided should be summarized in short sentences to facilitate the testing and scaling phases of the SBM design that are to come later.

The process we have depicted up to here covers Phases I and II by Busch et al. (2018). Thereafter, we need to turn social and environmental value creation for the stakeholders into a business opportunity. Hence, we reach the moment to embed the social and environmental concerns into economic value creation and to identify the potential sources of failure of our initial value proposition. To do so we propose to use table 2 below to summarize the main traits of the start-up value proposition and its main sources of failure. Thus, assuming that our initial thoughts can be wrong about who our key stakeholders are (their traits and their degree of importance for the start-up), and what they want and expect from the start-up to deliver (what type of value is important for them, the problems solved).

Table. 2. Value Proposition template.

|

What is your concept? Write here a name for your concept |

||

|

Who is it for? Write here the stakeholders to whom the value creation is addressed. The ones that without them the entrepreneurial project would never exist (include their main traits, use short sentences) |

What problem(s) does your concept solve? Write here the specific problem(s) your concept solves (use short sentences) |

What makes you different from the already existing solutions? Think of the concept's main attributes and how are different from other existing solutions. Highlight how social and environmental sources of value creation drive economic value creation. |

|

How does it work? Summarize the three previous cells into the first version of your value proposition. |

||

|

Why might it fail? Identify the possible sources of failure in your initial idea. Please be honest, that is the most important point of this step. |

What should we prototype and test? As a consequence of the previous cell, write the critical assumptions you made on the stakeholders, the type of value, and your solution that should be tested to minimize the odds of failure. |

How do we measure success/failure? As a consequence of the previous cell, write the possible metrics that could help to test your critical assumptions. |

|

Timeframe and steps to complete the testing process

Insert your timeline with your milestones |

||

Source: own elaboration

As we may observe in Table 2, which we called the Value proposition template, our purpose is not only to provide a template for a start-up on how to turn the sources of social and environmental value creation for its key stakeholders into a source of economic value creation to support its business model. But also, to provide support to minimize the odds of failure by identifying the possible sources of failure and how to test them and measure success and failure at the first stages of the project development. i.e., trying to prevent failure from the beginning and preparing for the next steps of development (testing and scaling). We will depict the next steps in the upcoming section 3.

3. Why test and scale SBM using the Lean Start-up method

At this point of the discussion, it is important to recall that, differently from businesses in operation, start-ups look for a repeatable and scalable business model. Therefore, entrepreneurs must accept that what they have is a series of untested hypotheses. The traditional literature on business model design proposes the use of the Business Model Canvas (BMC) in the case of ordinary business models economic value-centered (Osterwalder & Pigneur, 2010) or the Tripple layered Business Model Canvas (TLBMC) in the case of sustainable-driven projects (Joyce & Paquin, 2016) as the business model design tool of reference. Both fall into the category of “on-the-desk methods” because their assumptions are based on the entrepreneurial group's previous knowledge and background. In contrast, more recently, the Lean Start-up (LSU) approach has put at the center of the debate the importance of testing the key assumptions of the BM before proceeding with its definitive design (Blank, 2013). Then, LSU is also known as the “getting out of the building method” because it tests the essential assumptions on which the initial BM relies based on the feedback provided by potential users, purchasers, and other possible relevant partners (Bocken & Snihur, 2020).

Hence, the LSU methodology is based on agile development whose underlying idea consists of testing the essential assumptions and pivoting what did not work according to the feedback provided by a series of experiments conducted using “The Validation Board” (VB). Therefore, it is a method based on, both, a learning process, and data (Ries, 2011; Blank & Dorf, 2012).

However, up to date, the LSU method has only considered the steps to test and scale ordinary economic value-driven BM and has not been adapted to the requirements of the SBM (Sanchis, Campos, & Ejarque, 2020). Consequently, we propose to adapt the VB to the requirements that imply testing and scaling SBM. Table 3 below, shows the adapted version of the VB.

Table. 3. VB adapted to test and scale SBM.

|

|

Start |

1st Pivot |

2nd Pivot |

3rd Pivot |

4th Pivot |

|

Stakeholder hypotheses |

|

|

|

|

|

|

Problem hypotheses |

|

|

|

|

|

|

Solution hypotheses |

Not Applicable |

|

|

|

|

|

Core Assumptions About the solution hypotheses (1st and consecutive pivots) |

Riskiest assumption Point to the riskiest one, the one that will drive your idea to fail if not validated |

Get out of the building to get your results Design a questionnaire, pass it to the key stakeholders, and get feedback |

Invalidated List your invalidated hypotheses (Start) or invalidated core assumptions (1st and consecutive pivots) |

Validated List your validated hypotheses (Start) or validated core assumptions (1st and consecutive pivots) |

|

|

Method Delphi Method |

|||||

|

Minimum Success Criterion To be set at any iteration |

|||||

Source: own elaboration

As we can observe in Table 3, the process begins at the “start” column testing the hypotheses we made on stakeholders (who they are and their preferences) and the problems they have. Our proposal, differently from the original VB, is stakeholder-centered instead of customer-centered. Moreover, in terms of problems, our proposal takes into consideration all kinds of problems. Therefore, it involves social and environmental concerns. Thus, widening the potential range for value creation and the stakeholders served following Busch et al. (2018).

In addition, to work with testing and scaling methodology based on data we introduce another variation to the VB. Hence, when it comes to defining the method to use in the hypotheses and core assumption testing, we propose to base the testing process on the Delphi method. The Delphi method is a prospective technique based on expert consultation utilizing a questionnaire (Landeta, 2006; Castilla-Polo et al., 2020). For our purposes, the experts to be consulted will be the key stakeholders we identified in Table 1. So, we pass the questionnaire to a sample of the key stakeholder groups showing the same profile as the one depicted in Table 1. To design the questionnaire, we will take Tables 2 and 3 as a reference and will count with the support of Table 4 below.

Table. 4. Delphi questionnaire support.

|

Hypothesis |

Assumption |

Riskiest? |

Question/s to test the Hypothesis |

Minimum success criterion |

|||

|

Stakeholder |

Problem |

Solution |

Yes |

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source: own elaboration

Thereafter, we will pass the Delphi questionnaire to the sample of key stakeholders and assess their answers in terms of the median of their responses as the measure that reflects the group’s opinion and the interquartile rank as the measure for the degree of agreement among the individuals of the same stakeholder group (Landeta & Barrutia, 2011). Following the Delphi method will facilitate the setting up of the minimum success criterion to validate or invalidate any of the hypotheses and core assumptions we previously made. This process is to be performed in some iterations until all the hypotheses and core assumptions on which our initial SBM relies are validated or redefined (Bocken & Snihur, 2020; Johnson & Schaltegger, 2020).

4. Full design of a scalable Sustainable Business Model using the Tripple Layered Business Model Canvas

Once we have validated all the hypotheses and core assumptions on which our SBM is based, the SBM is scalable and we can proceed with its full design using the TLBMC. According to Joyce & Paquin (2016), the TLBMC consists of a three-layer BM canvas with a social, environmental, and economic layer to be used to support the SBM design.

Such a tool is conceived to keep vertical coherence among its three layers, thus, the starting point to proceed with the SBM design is the social layer, followed by the environmental, and, finally the economic one. This procedure is in line with the system change process described by (Busch, Hamprecht, & Waddock, 2018).

In addition, the TLBMC also keeps horizontal coherence within every one of the three layers. Then, it ensures the overall model coherence.

Therefore, we will begin the SBM full design with the social layer depicted in Table 5 below.

Table. 5. The social layer of the TLBMC.

|

Local Communities

|

Governance

|

Social Value |

Societal Culture

|

End-User |

|

Employees

|

Scale of Outreach

|

|||

|

(-) Social Impacts

|

(+) Social Benefits |

|||

Source: Joyce & Paquin (2016).

Table 5 depicts the overall social value created coming from the business operation, this includes identifying and quantifying the positive and negative social impacts. Then, this layer allows a full SBM design because, in the design step, the entrepreneurial group is completely aware of their social impact and the sources of that impact. So, by changing the design they can minimize the negative impact and maximize the social benefits of their start-up.

Thereafter, we will follow by completing the environmental layer of the TLBMC. Table 6 below, depicts it. Such layer takes life-cycle assessment as a reference to identify and design the BM in environmental terms. Thus, allowing the entrepreneurial group to configure all the activities of their SBM maximizing the positive environmental benefits and minimizing the negative impacts.

Table. 6. The environmental layer of the TLBMC.

|

Supplies and Outsourcing

|

Production

|

Environmental Value |

End-of-life |

User Phase |

|

Materials

|

Distribution |

|||

|

(-) Environmental Impacts

|

(+) Environmental Benefits |

|||

Source: Joyce & Paquin (2016).

Finally, the last layer to be designed is the economic one. Table 7 below shows the economic layer that basically works in the way described by Osterwalder & Pigneur (2010). However, as we are dealing with the design of SBM, every cell of the economic layer must keep its coherence with the equivalent cell of the environmental and social layers (Joyce & Paquin, 2016).

Table. 7. The economic layer of the TLBMC.

|

Partners |

Activities

|

Value Proposition |

Customer Relationship

|

Customer Segments |

|

Resources

|

Channels

|

|||

|

Costs

|

Revenues |

|||

Source: Joyce & Paquin (2016).

5. Conclusions

The present work had as its main aim was to propose a sequential and combined method to design, test, and scale SBM integrating sustainability concerns through the ECG framework, as we did in section 2. In addition, to test the hypotheses and core assumptions we made initially we relied on LSU. However, to keep a multi-stakeholder sustainable approach and make the value creation process wider, we introduced some changes to the LSU initially designed by Ries (2011).

Likewise, in an attempt to make our testing process more objective and data-driven, our adaptation proposes to test the hypotheses and core assumptions using a prospective technique: the Delphi method. This allowed systematizing the part of the SBM design that is less creative, i. e. the testing of the hypotheses and the core assumptions.

Finally, our sequential methodology takes the results of the LSU based on the Delphi method as a reference and completes the full SBM design using the TLBM. Thus, keeping the coherence between the contrast of the core assumptions and hypotheses on which the SBM relied and the full SBM design. This way we try to minimize the risk of failure by building the full SBM design on validated and data-driven knowledge.

This sequential and combined methodology has been tested over five consecutive years with students enrolled in an Entrepreneurship course at the University of València, including local and international students. Their experience and ours are completely positive.

Social and environmental value creation was embedded into the BM since the beginning of the process through the ECG framework. LSU, using the Delphi method, is applied to test the underlying hypotheses and core assumptions. TLBMC closes the loop allowing a complete design of SBM based on contrasted assumptions.

The combination of the sustainable approach provided by the ECG framework and the TLBMC with the “getting out of the building” approach provided by the LSU model, and the data-driven approach provided by the Delphi method working sequentially, allows taking advantage of some synergies. Thus, overcoming the limitations of the three methodologies applied by separate whilst integrating sustainability concerns into the BM from the initial stages.

Finally, we have developed the present teaching methodology in the classrooms of the Faculty of Economics at the University of València, and with the active participation of our students to whom it was addressed. Therefore, our approach is eminently practice-driven and action-based. After five years of scaling this teaching methodology, our will is to share it with our colleagues to keep the door open for its future development.

Conflict of interest: The authors declare no conflict of interest regarding the contents disclosed in the present paper. No funding was received.

Authors’ contribution roles: All authors have contributed equally to conceptualizing, formal analysis, investigation, and project administration.

6. References

Betáková, J., Havierniková, K., Okręglicka, M., Mynarzova, M., & Magda, R. (2020). The role of universities in supporting entrepreneurial intentions of students toward sustainable entrepreneurship. Entrepreneurship and Sustainability Issues, 8(1), pp. 573-589. https://doi.org/10.9770/jesi.2020.8.1(40).

Birkin, F., Polesie, T., & Lewis, L. (2009). A new business model for sustainable development: an exploratory study using the theory of constraints in Nordic organizations. Business Strategy and the Environment, 18(5), pp. 277-290. https://doi.org/10.1002/bse.581.

Blank, S. (2013). Why the lean start-up changes everything. Harvard Business Review. 91(5), pp. 63-72.

Blank, S., & Dorf, B. (2012) The Startup Owner's Manual (First ed.). New Jersey: K & S Ranch Publishing.

Bocken, N., & Snihur, Y. (2020) Lean Startup and the business model: experimenting for novelty and impact. Long Range Planning, 53(1), pp. 1-9. https://doi.org/10.1016/j.lrp.2019.101953.

Busch, T., Hamprecht, J., & Waddock, S. (2018) Value(s) for Whom? Creating Value(s) for Stakeholders. Organization & Environment, 31(3), pp. 210-222. https://doi.org/10.1177/1086026618793962.

Campos Climent, V. (2016) La economía social y solidaria en el siglo XXI: un concepto en evolución. Cooperativas, B corporations y economía del bien común. Oikonomics. Revista de Economía, Empresa y Sociedad, 6, pp. 6-15.

Campos, V., Sanchis, J., & Ejarque, A. (2020) Social entrepreneurship and Economy for the Common Good: Study of their relationships through a bibliometric analysis. The International Journal of Entrepreneurship and Innovation, 21(3), pp. 156-167. https://doi.org/10.1177/1465750319879632.

Carroll, A. B. (1991) The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4), pp. 39-48.

Castilla-Polo, F.; Ruiz-Rodríguez, M.C.; Delgado-Marfil, C. (2020) La técnica Delphi para la validación de escalas de medida: las variables innovación y reputación dentro de almazaras cooperativas. REVESCO. Revista de Estudios Cooperativos, vol. 136, e71852. https://dx.doi.org/10.5209/reve.71852.

Dean, T. J., & McMullen, J. S. (2007) Toward a theory of sustainable entrepreneurship: Reducing environmental degradation through entrepreneurial action. Journal of Business Venturing, 22(1), pp. 50-76. https://doi.org/10.1016/j.jbusvent.2005.09.003.

Donaldson, T., & Walsh, J. (2015) Toward a theory of business. Research in Organizational Behavior, 35, pp. 181-207. https://doi.org/10.1016/j.riob.2015.10.002.

Drucker, P. (1955) The Practice of Management. Allied publishers.

Dyllick, T., & Hockerts, K. (2002) Beyond the business case for corporate sustainability. Business Strategy and the Environment, 11(2), pp. 130-141. https://doi.org/10.1002/bse.323.

Dyllick, T., & Muff, K. (2016) Clarifying the Meaning of Sustainable Business: Introducing a Typology From Business-as-Usual to True Business Sustainability. Organization & Environment, 29(2), pp. 156-174. https://doi.org/10.1177/1086026615575176.

Ejarque, A., & Campos, V. (2020) Assessing the Economy for the Common Good Measurement Theory Ability to Integrate the SDGs into MSMEs. Sustainability, 12(24), 10305. https://doi.org/10.3390/su122410305.

Elkington, J. (1994) Towards the sustainable corporation: win-win-win business strategies for sustainable development. California Management Review, 36(2), 90.

Elkington, J. (2004) Enter the triple bottom line. The triple bottom line. Does it all add up, 11(12) pp. 1-16.

Engert, S., Rauter, R., & Baumgartner, R. J. (2016) Exploring the integration of corporate sustainability into strategic management: a literature review. Journal of Cleaner Production, 112, pp. 2833-2850. https://doi.org/10.1016/j.jclepro.2015.08.031.

Falle, S., Rauter, R., Engert, S., & Baumgartner, R. J. (2016) Sustainability management with the sustainability balanced scorecard in SMEs: Findings from an Austrian case study. Sustainability, 8(6), 545. https://doi.org/10.3390/su8060545.

Felber, C. (2010). Change everything: Creating an economy for the common good. Zed Books Ltd.

Felber, C., Campos, V., & Sanchis, J. (2019) The Common Good Balance Sheet, an Adequate Tool to Capture Non-Financials? Sustainability, 11(14), 3791. https://doi.org/10.3390/su11143791.

Figge, F., Hahn, T., Schaltegger, S., & Wagner, M. (2002) The Sustainability Balanced Scorecard- Theory and application of a tool for value-based sustainability management, Gothenburg Greening of Industry Network Conference, pp. 1-32.

Freeman, R. (1984) Strategic Management: A Stakeholder approach. Boston, MA: Pitman.

Freeman, R. (2008) Ending the so-called "Friedman-Friedman" debate. Business Ethics Quarterly, 18, pp. 153-190.

Freeman, R., Wicks, A., & Parmar, B. (2004) Stakeholder theory and "the corporate objective revisited". Organisation Science, 15, pp. 364-369. https://doi.org/10.1287/orsc.1040.0066.

Giesenbauer, B., & Müller-Christ, G. (2018) Die Sustainable Development Goals für und Durch KMU. Ein Leitfaden. Bremen, Germany: Universität Bremen.

Guzmán, A., & Trujillo, M. A. (2008) Social Entrepreneurship–Literature Review. Estudios gerenciales, 24(109), pp. 109-219.

Hörisch, J., Freeman, R., & Schaltegger, S. (2014) Applying stakeholder theory in sustainability management: Links, similarities, dissimilarities, and conceptual framework. Organization & Environment, 27, pp. 328-346. https://doi.org/10.1177/1086026614535786.

Johnson, M. P., & Schaltegger, S. (2016). Two decades of sustainability management tools for SMEs: How far have we come?. Journal of Small Business Management, 54(2), pp. 481-505. https://doi.org/10.1111/jsbm.12154.

Johnson, M., & Schaltegger, S. (2020) Entrepreneurship for Sustainable Development: A Review and Multilevel Causal Mechanism Framework. Entrepreneurship Theory and Practice., 44(6), pp. 1141-1173. https://doi.org/10.1177/1042258719885368.

Joyce, A., & Paquin, R. L. (2016) The triple layered business model canvas: a tool to design more sustainable business models. Journal of Cleaner Production., 135, pp. 1474-1486. https://doi.org/10.1016/j.jclepro.2016.06.067.

Ketola, T. (2010) Five leaps to corporate sustainability through a corporate responsibility portfolio matrix. Corporate Social Responsibility & Environmental Management, 17, pp. 320-336. https://doi.org/10.1002/csr.219.

Klewitz, J. y Hansen, E. G. (2014). Sustainability-oriented innovation of SMEs: A systematic review. Journal of Cleaner Production, 65, pp. 57-75. https://doi.org/10.1016/j.jclepro.2013.07.017.

Landeta, J. (2006) Current validity of the Delphi method in social sciences. Technological forecasting and social change, 73(5), pp. 467-482. https://doi.org/10.1016/j.techfore.2005.09.002.

Landeta, J., & Barrutia, J. (2011) People consultation to construct the future: a Delphi application. International Journal of Forecasting, 27(1), pp. 134-151. https://doi.org/10.1016/j.ijforecast.2010.04.001.

Meseguer-Sánchez, V., Gálvez-Sánchez, F. J., López-Martínez, G., & Molina-Moreno, V. (2021) Corporate Social Responsibility and Sustainability. A Bibliometric Analysis of Their Interrelations. Sustainability, 13(4), 1636. https://doi.org/10.3390/su13041636.

Moya-Clemente, I., Ribes-Giner, G., & Chaves-Vargas, J. C. (2021) Sustainable entrepreneurship: an approach from bibliometric analysis. Journal of Business Economics and Management, 22(2), pp. 297-319. https://doi.org/10.3846/jbem.2021.13934.

Murillo Pérez, L.M. (2022). ¿Cómo genera valor el emprendimiento social de inclusión socio-laboral? Propuesta metodológica para la identificación y análisis de buenas prácticas. REVESCO. Revista de Estudios Cooperativos, vol. 140, e78927. https://dx.doi.org/10.5209/reve.78927.

Osterwalder, A., & Pigneur, Y. (2010) Business Model Generation: a Handbook for Visionaries, Game Changers and Challengers. John Willey & Sons.

Osterwalder, A., Pigneur, Y., & Tucci, C. (2005). Clarifying business models: origins, present, and future of the concept. Communications of the Association for Information Systems, 15, pp. 1-25. https://doi.org/10.17705/1CAIS.01601.

Parmar, B., Freeman, R., Harrison, J., Wicks, A., Purnell, L., & De Colle, S. (2010) Stakeholder theory: The state of the art. Academy of Management Annals, 4, pp. 403-445. https://doi.org/10.5465/19416520.2010.495581.

Pinelli, M., & Maiolini, R. (2017) Strategies for sustainable development: Organizational motivations, stakeholders' expectations and sustainability agendas. Sustainable Development, 25(4), pp. 288-298. https://doi.org/10.1002/sd.1653.

Porter, M. E., & Kramer, M. (2011) The Big Idea: Creating Shared Value. How to Reinvent Capitalism—and Unleash a Wave of Innovation and Growth. Harvard Business Review, 89(1-2), pp. 62-77. https://link.springer.com/chapter/10.1007/978-94-024-1144-7_16.

Ries, E. (2011) The Lean Startup (Fisrt ed.). New York: Crown Business.

Sachs, J. D. (2012) From millennium development goals to sustainable development goals. The Lancet, 379(9832), pp. 2206-2211. https://doi.org/10.1016/S0140-6736(12)60685-0.

Sanchis, J. R., & Campos, V. (2019) The economy for the common good model: an organizational approach and bibliometric analysis. Estudios Gerenciales, 35(153), pp. 440-450. https://doi.org/10.18046/j.estger.2019.153.3361.

Sanchis, J. R., Campos, V., & Ejarque, A. (2020) Emprendimiento Sostenible. Emprendiendo desde la cocreación de valor y el bien común. Madrid: Piramide.

Schaltegger, S. (2014) A Framework for Ecopreneurship. Greener Management International, 38, pp. 45-58.

Schaltegger, S., Beckmann, M., & Hockerts, K. (2018) Collaborative entrepreneurship for sustainability. Creating solutions in light of the UN sustainable development goals. International Journal of Entrepreneurial Venturing, 10(2), pp. 131-152.

Schaltegger, S., Hansen, E. G., & Lüdeke-Freund, F. (2016) Business models for sustainability: Origins, present research, and future avenues. Organization & Environment, 29(1), pp. 3-10.

Schaltegger, S., & Lüdeke-Freund, F. (2011) The sustainability balanced scorecard: Concept and the case of Hamburg airport. Centre for Sustainability Management (CSM), Leuphana Universität Lüneburg. https://ssrn.com/abstract=2062320.

Schaltegger, S., Lüdeke-Freund, F., & Hansen, E. G. (2011) Business cases for sustainability and the role of business model innovation: developing a conceptual framework. Centre for Sustainability Management (CSM), Leuphana Universität Lüneburg. https://ssrn.com/abstract=2010506.

Schaltegger, S., & Wagner, M. (2011) Sustainable entrepreneurship and sustainability innovation: Categories and interactions. Business Strategy and the Environment, 20(4), pp. 222-237. https://doi.org/10.1002/bse.682.

Somekh, B. (2005) Action Research. UK: McGraw-Hill.

Stubbs, W., & Cocklin, C. (2008) Conceptualizing a ''sustainability business model''. Organization & Environment, 21(2), pp. 103-127. https://doi.org/10.1177/1086026608318042.

Trimi, S., & Berbegal-Mirabent, J. (2012) Business model innovation in entrepreneurship. International Entrepreneurship and Management Journal, 8(4), pp. 449-465. https://doi.org/10.1007/s11365-012-0234-3.

Zahra, S., Gedajlovic, E., Neubaum, D., & Shulman, J. (2009) A typology of social entrepreneurs: Motives, search processes and ethical challenges”. Journal of Business Venturing, 24(5), pp. 519-531.